5 Key Benefits of RPA in Banking That Changed Financial Workflows

Explore the benefits of RPA in banking, where automation delivers value, where limits appear, and how real-time voice AI turns workflows into live execution.

Calls keep stacking up, customers switch languages mid-conversation, and your ops team is stuck stitching together systems that were never designed to talk in real time. That is usually when teams start looking into the benefits of RPA in banking, hoping automation can finally bring structure to chaotic workflows. With the global market size of RPA in banking expected to reach around USD 6.9 billion by 2032, it is clear that automation is becoming core infrastructure, not an experiment. Still, many teams discover that the benefits of RPA in banking solve only part of the operational pressure once live conversations enter the picture.

What banking leaders actually want is automation that handles real interactions, not only background tasks. Voice-driven workflows, low-latency execution, and systems that react while a call is happening are quickly replacing static automation expectations. The shift is less about replacing what already works and more about extending it into real-time engagement where customers, risk signals, and operations meet.

In this guide, we take a look at where RPA delivered value, where it hits limits, and how modern AI layers push banking automation into autonomous workflows.

Key Takeaways

RPA Built The Operational Foundation: Banks adopted RPA to stabilize reconciliation, reporting, compliance logging, and batch workflows, creating predictable execution layers across legacy banking infrastructure.

Automation Limits Appear In Live Conversations: Structured bots struggle when servicing shifts into voice interactions, multilingual intent changes, or real-time negotiation flows that require contextual reasoning.

Voice AI Extends Automation Into Execution Time: Real-time speech models allow banking workflows to trigger during calls, turning conversations into active operational touchpoints instead of post-call processing tasks.

Architecture Is Moving Toward Asynchronous Models: Multi-modal systems process speech, data, and backend events simultaneously, replacing sequential pipelines that slow down customer-facing operations.

Real-Time Voice Infrastructure Is Becoming Core Banking Tech: Platforms like Smallest AI combine low-latency speech, full-duplex interaction, and developer-ready orchestration to modernize automation without replacing legacy systems.

What RPA Means for Banking Operations Today

RPA sits inside core banking stacks as an execution layer that moves data across legacy systems, reduces manual queue handling, and standardizes operational throughput without rewriting mainframe infrastructure.

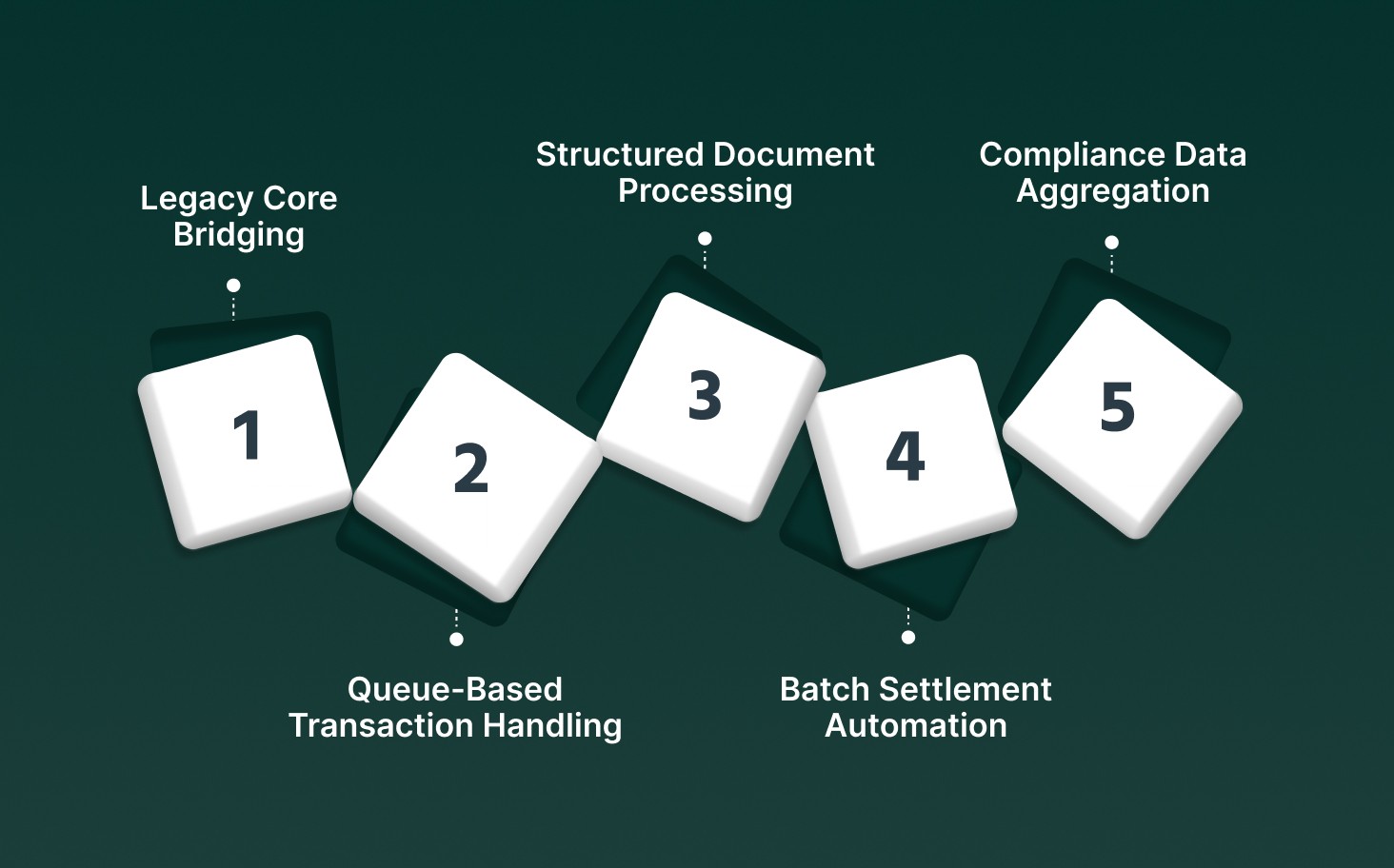

Modern banking teams rely on RPA across specific operational layers where structured workflows dominate, and deterministic execution matters most.

Legacy Core Bridging: Bots trigger COBOL or mainframe screens through UI automation, syncing transaction data between core banking systems and modern CRM or ERP platforms without backend rewrites.

Queue-Based Transaction Handling: RPA monitors SWIFT queues, reconciliation backlogs, and payment exceptions, routing structured cases to downstream systems using predefined rule trees and audit logs.

Structured Document Processing: OCR pipelines extract fields from KYC forms, loan disclosures, and compliance reports, validating schema formats before pushing records into underwriting workflows.

Batch Settlement Automation: End-of-day settlement files, ACH batches, and ledger updates run through scheduled bot orchestration, reducing overnight operational staffing requirements.

Compliance Data Aggregation: Bots collect transaction metadata across AML tools, risk engines, and reporting systems to generate regulator-ready datasets without manual spreadsheet consolidation.

RPA today functions as the execution engine behind structured banking workflows, stabilizing operational throughput while legacy systems remain in place.

See how real-time voice automation fits into modern customer operations with Call Center Automation: Complete Guide to Tools, Benefits, and Implementation

5 Core Benefits of RPA in Banking That Drove Early Adoption

Banks adopted RPA to stabilize high-volume back-office execution, reduce processing delays, and introduce predictable operational throughput across regulated workflows without replacing legacy banking infrastructure.

Cost Reduction Through Process Automation

Early deployments targeted repetitive workflows like reconciliation, settlements, and document handling, where deterministic automation reduced manual overhead while keeping existing operational systems intact.

Reconciliation Cycle Automation: Bots validate ledger mismatches across treasury systems, reducing analyst intervention during daily balance checks and minimizing overtime tied to manual financial reviews.

Payment Processing Execution: Automated clearing workflows handle card settlement updates and internal transfer confirmations without requiring manual queue monitoring or repetitive system navigation across operations teams.

Back Office Reporting Generation: Regulatory reporting datasets compile automatically from transaction logs, eliminating manual spreadsheet consolidation that historically slowed quarterly financial reporting cycles.

How banking ops actually feel that change today: Teams experience fewer overnight backlogs and reduced manual escalation queues, allowing analysts to focus on exception handling instead of repetitive operational verification work.

Where pressure points still exist: Complex workflows with conversational context or unstructured communication still require human intervention, limiting full automation benefits across servicing, collections, and customer engagement functions.

Elimination Of Human Error And Increased Accuracy

RPA introduced deterministic rule execution into banking processes, removing variability in data handling and improving operational consistency across transaction processing, compliance checks, and financial reporting pipelines.

Data Field Validation Controls: Bots enforce schema-level checks across customer onboarding datasets, preventing missing identity fields or incorrect formatting from progressing into downstream compliance systems.

Transaction Matching Logic: Automated reconciliation scripts compare internal ledgers against clearinghouse feeds, identifying mismatches instantly rather than waiting for manual end of day review cycles.

Exception Workflow Routing: Structured rule engines escalate discrepancies directly into risk review queues, reducing delays caused by manual triage processes across operations departments.

How banking ops actually feel that change today: Analysts trust baseline transaction accuracy more, spending time reviewing flagged anomalies instead of rechecking routine records that previously required multiple manual verification passes.

Where pressure points still exist: Rule-based logic struggles when customer intent shifts mid-interaction or when contextual decision flows require interpretation beyond structured data fields and predefined validation paths.

Smooth Regulatory Compliance And Risk Management

Banks adopted RPA to standardize regulatory reporting processes, maintain detailed activity logs, and automate surveillance workflows tied to AML monitoring, KYC verification, and risk governance obligations.

Automated Audit Trail Generation: Every system action logs automatically with timestamps and execution context, simplifying regulator review processes and reducing time spent compiling compliance evidence manually.

Sanctions Screening Execution: Bots cross-reference customer records against watchlists and sanctions databases at scale, accelerating onboarding checks without expanding compliance staffing requirements.

Risk Reporting Compilation: RPA aggregates transaction-level risk data into standardized reporting formats required for internal governance and external regulatory submissions.

How banking ops actually feel that change today: Compliance teams shift from manual documentation gathering toward oversight roles, monitoring automated workflows rather than assembling regulatory datasets from multiple disconnected systems.

Where pressure points still exist: Real-time customer conversations and nuanced negotiation scenarios still sit outside structured automation, creating blind spots in workflows where regulatory context emerges dynamically.

Improved Customer Experience And Operational Speed

Early automation focused on reducing turnaround time for operational tasks that impacted customers indirectly, compressing processing windows for onboarding, servicing updates, and internal approval cycles.

Digital Onboarding Processing: Bots validate application data against identity databases, pushing approved profiles into account provisioning systems without waiting for manual document verification steps.

Loan Approval Workflow Acceleration: Structured eligibility checks run automatically across credit scoring models and internal rule engines, reducing approval cycle durations for retail lending teams.

Account Maintenance Updates: Change requests like address updates or service modifications execute automatically across multiple internal systems, removing delays tied to manual data replication.

How banking ops actually feel that change today: Service teams handle fewer internal status requests since backend workflows complete faster, reducing follow-up calls triggered by slow processing timelines.

Where pressure points still exist: Customer-facing voice interactions remain manual, limiting end-to-end speed gains once conversations or negotiations become part of the servicing workflow.

Instant Scalability Across Transaction Volumes

RPA allowed banks to expand operational capacity during peak periods by deploying additional automation instances rather than increasing headcount, stabilizing throughput during seasonal or market-driven surges.

High Volume Payment Processing: Additional bot instances process bulk payment batches during settlement peaks, preventing transaction queues from extending into next-day processing cycles.

Market Event Workflow Expansion: Automation handles surges in account updates or trading-related documentation during volatile market periods without increasing manual staffing pressure.

Back Office Workload Distribution: Bot orchestration platforms dynamically allocate tasks across automation nodes, balancing workloads without manual resource scheduling.

How banking ops actually feel that change today: Operations managers rely less on temporary staffing during peak cycles, maintaining service levels without sudden hiring or overtime planning during volume spikes.

Where pressure points still exist: Scaling conversational workflows remains difficult because traditional RPA cannot interpret speech, intent, or emotional context required during complex customer interactions.

Early RPA adoption delivered predictable gains across structured banking workflows, yet operational impact plateaus once processes shift from deterministic execution into real-time human conversations and dynamic decision flows.

Build real-time voice automation that listens, responds, and executes workflows instantly with Smallest AI’s ultra-low latency speech models, full-duplex interaction, and on-prem deployment flexibility.

The Next Layer of Banking Automation: Real-Time Voice AI Agents

Banking automation is shifting from workflow execution toward real-time conversational intelligence, where speech-native models process intent, context, and interruptions while interacting directly with customers across voice channels.

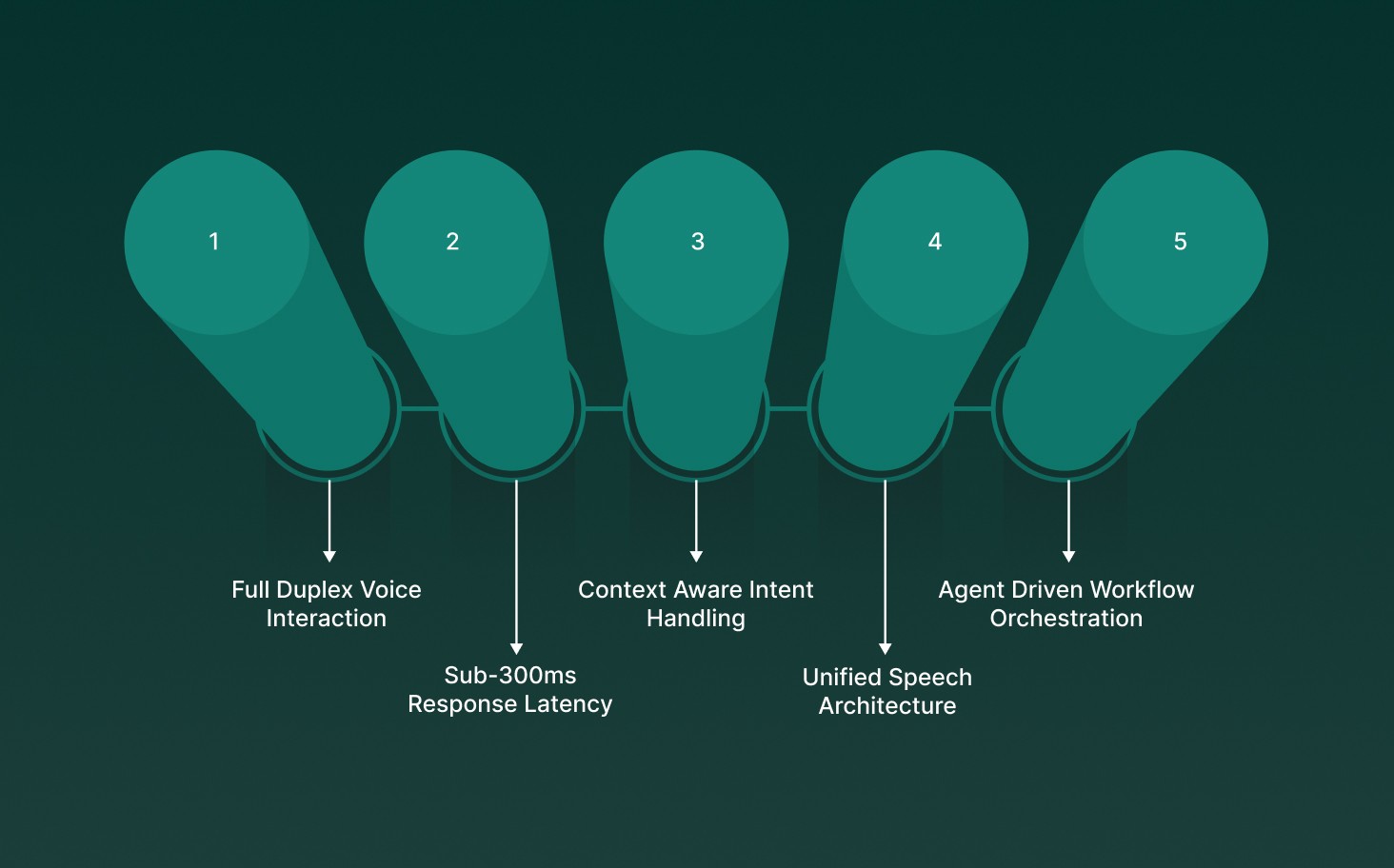

Operational shifts appear when banks deploy voice AI agents that combine low-latency speech models, conversational reasoning, and system orchestration to handle interactions that traditional automation cannot interpret.

Full Duplex Voice Interaction: Agents listen and respond simultaneously, keeping conversations natural even when customers interrupt or change direction mid-call.

Sub-300ms Response Latency: Faster inference keeps servicing flows smooth, preventing delays that break conversation rhythm during authentication, negotiations, or support calls.

Context Aware Intent Handling: Voice models recognize language switches, tone changes, and partial phrases, updating backend workflows in real time without manual intent tagging.

Unified Speech Architecture: End-to-end voice models reduce pipeline complexity, improving stability during high-volume inbound or outbound campaigns.

Agent Driven Workflow Orchestration: Live conversations trigger CRM updates, payment actions, and compliance checks instantly, turning calls into active execution channels.

Real-time voice AI agents extend automation into live customer interactions, allowing banks to automate conversations with the same precision once reserved for structured backend workflows.

Explore how real-time conversational automation is reshaping customer interactions in 6 High-Impact AI Chatbot Use Cases Transforming Banking in 2026

Architecture Shift: From Static Bots to Asynchronous Multi-Modal Models

Banking automation architecture is moving away from UI-driven bots toward speech-native, multi-modal models that process voice, text, and events asynchronously while orchestrating workflows across enterprise systems in real time.

Architectural differences between legacy automation stacks and asynchronous multi-modal models reveal how banking platforms are transitioning from rigid execution layers into continuously adaptive conversational infrastructure.

Architecture Dimension | Static Bots (Legacy Automation) | Asynchronous Multi-Modal Models |

Execution Model | Sequential workflows are triggered step-by-step through rigid rule chains. | Event-driven pipelines process speech, intent, and system signals concurrently without waiting for sequential task completion. |

Data Processing Layer | Structured field inputs only, dependent on predefined UI selectors and fixed schemas. | Multi-modal ingestion supports voice streams, conversational context, and API events within a unified inference loop. |

Latency Profile | High cumulative delays are caused by transcription, processing, and response layers running independently. | Unified speech models reduce cascading overhead, allowing continuous conversational flow during real-time customer interactions. |

Context Management | Stateless execution resets after each workflow trigger, limiting adaptability mid-process. | Persistent memory layers maintain conversational and operational state across channels, allowing dynamic decision adjustments during live interactions. |

Scalability Approach | Scaling requires replicating bot instances tied to specific workflows or applications. | Horizontal scaling distributes inference workloads across asynchronous compute nodes without duplicating entire workflow logic stacks. |

Asynchronous multi-modal architectures transform banking automation from static execution engines into continuous interaction systems, allowing real-time decision flows across voice, data, and operational events simultaneously.

See how automation extends across compliance, servicing, and real-time operations in Top 16+ RPA Use Cases Transforming the Banking Industry

Future Outlook: From RPA Benefits to Autonomous Banking Workflows

Banking automation is shifting toward autonomous workflows where AI agents interpret intent, trigger systems, and execute decisions continuously without manual workflow initiation.

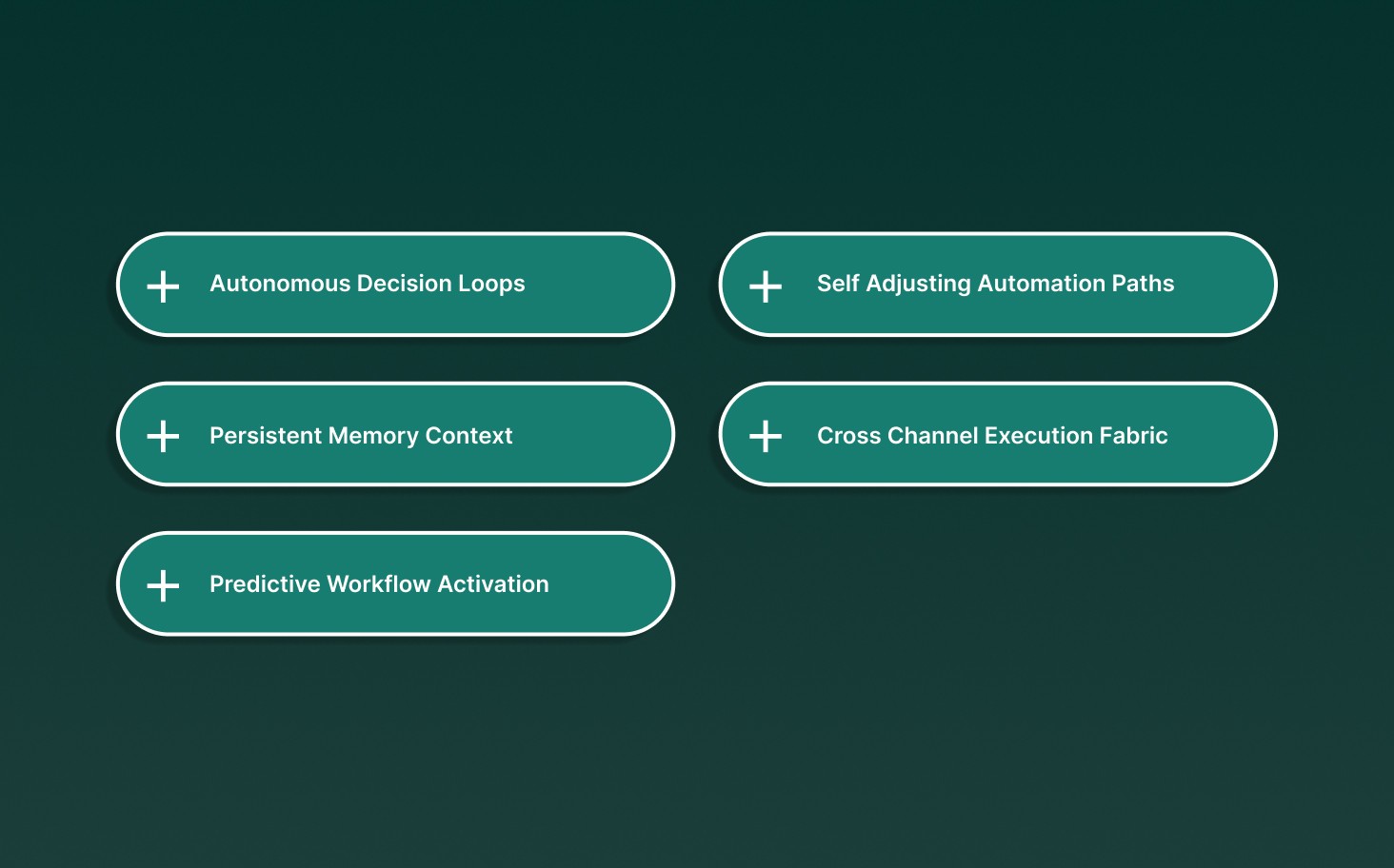

Future progression centers on automation layers that move from rule execution toward adaptive orchestration across live interactions, operational signals, and backend banking systems.

Autonomous Decision Loops: Agents monitor repayment behavior and transaction signals continuously, triggering actions without waiting for manual approvals or batch-driven workflows.

Persistent Memory Context: Automation retains conversation history across channels, allowing follow-ups without repeating identity checks or restarting servicing flows.

Predictive Workflow Activation: Models anticipate servicing needs or risk signals early, allowing automation to initiate outreach before queues or delinquencies escalate.

Self Adjusting Automation Paths: Escalations, communication cadence, and workflow routing shift dynamically based on live interaction signals instead of fixed scripts.

Cross Channel Execution Fabric: Unified orchestration connects voice, chat, and backend events so operational actions execute instantly, regardless of how customers engage.

Autonomous workflows extend automation beyond task execution, allowing banks to operate through continuous AI-driven coordination that blends decision intelligence with real-time operational execution across systems.

Where Smallest AI Fits Into Modern Banking Automation

Smallest AI brings real-time voice AI into banking automation, letting teams run conversations through ultra-low latency speech models without changing existing infrastructure or compliance workflows.

Deployment focuses on turning live speech into an execution layer that connects voice intelligence directly with backend banking systems during customer interactions.

Lightning TTS Voice Generation: Hyper-realistic speech synthesis delivers emotionally aware voice responses across 30+ languages, supporting collections, servicing, and multilingual outreach without scripted audio pipelines.

Pulse STT Speech Intelligence: Sub-70ms transcription with emotion detection and speaker labeling captures live conversational signals, allowing real-time operational triggers instead of post-call analysis workflows.

Hydra Full Duplex Engine: Unified speech-to-speech architecture processes listening and speaking simultaneously, removing serial processing delays and maintaining natural conversation flow during high-volume call handling.

On-Prem Deployment Flexibility: Banking teams deploy speech models locally to maintain data sovereignty, guaranteeing sensitive customer interactions stay within regulated infrastructure environments.

Developer Ready Voice Infrastructure: Node and Python SDKs allow teams to connect voice agents directly with CRM systems, payment gateways, and internal orchestration tools without rebuilding existing automation layers.

Smallest AI turns voice into a real-time automation interface, helping banks extend existing workflows into live conversations while maintaining speed, compliance, and operational control across regulated environments.

Final Thoughts!

Banking automation is entering a phase where speed and context matter as much as process control. The conversation is shifting from how many tasks can be automated to how naturally systems can respond while operations are still unfolding. Teams are rethinking what automation should feel like during real customer interactions, not only inside backend workflows. The next wave will belong to banks that design automation around live signals instead of static triggers.

If your automation stack is starting to feel rigid while customer conversations keep getting more complex, this is where real-time voice infrastructure changes the equation. Smallest AI gives teams the ability to run intelligent voice interactions without rebuilding their core systems or slowing down deployment cycles. From ultra-low latency speech to full duplex conversational models, the platform is built for operations that need precision at scale.

Explore how Smallest AI can power real-time banking automation that actually keeps up with your workflows. Get in touch with us!

What are some lesser-known benefits of robotic process automation in banking beyond cost savings?

How does the scope of RPA in banking extend beyond back-office workflows?

Can the benefits of robotic process automation in banking support multilingual customer operations?

What operational challenges limit the scope of RPA in banking today?

Are there compliance advantages tied to the benefits of robotic process automation in banking?