6 High-Impact AI Chatbot Use Cases Transforming Banking in 2026

Learn how banks use AI chatbots in banking to cut service load, handle voice calls, manage risk, and scale support with control, compliance, and ROI in 2026.

A customer calls to report a failed payment. The IVR loops. The agent asks for details that the app already knows. The issue gets resolved, but the experience leaves friction on both sides. Situations like this play out thousands of times a day across banks, quietly increasing service costs and customer dissatisfaction. That reality is why AI chatbots in banking have shifted from pilot projects to production systems tied directly to core operations.

For teams responsible for service quality, risk, and scale, AI chatbots in banking represent a structural change in how routine interactions are handled. They absorb high-volume requests, apply policy-bound logic, and route exceptions with precision. The investment signals are clear. By 2033, the market is forecasted to reach USD 14.12 billion, as banks increasingly use advanced chatbot solutions to improve operational efficiency, customer engagement, and fraud prevention.

In this guide, we will explain where AI chatbots deliver real operational value, examine proven banking use cases, evaluate voice-based deployments, unpack risk and compliance considerations, and outline how banks can balance automation with human expertise as adoption accelerates.

Key Takeaways

Operational, Not Experimental: AI chatbots in banking now run core service workflows tied directly to ledgers, LOS, fraud systems, and CRMs.

ROI Comes From Deterministic Automation: Measurable returns appear when chatbots replace rule-bound, high-volume tasks rather than acting as open-ended conversational assistants.

Voice AI Changes Call Economics: Real-time voice chatbots handle live calls at scale with low latency, controlled flows, and audit-ready interaction logs.

Risk Is a System Design Problem: Compliance failures stem from weak controls, not AI itself, requiring policy-bound responses, verification layers, and replayable decision paths.

Human Oversight Remains Structural: Successful banks embed escalation, confidence thresholds, and human approval into chatbot workflows for high-risk intents.

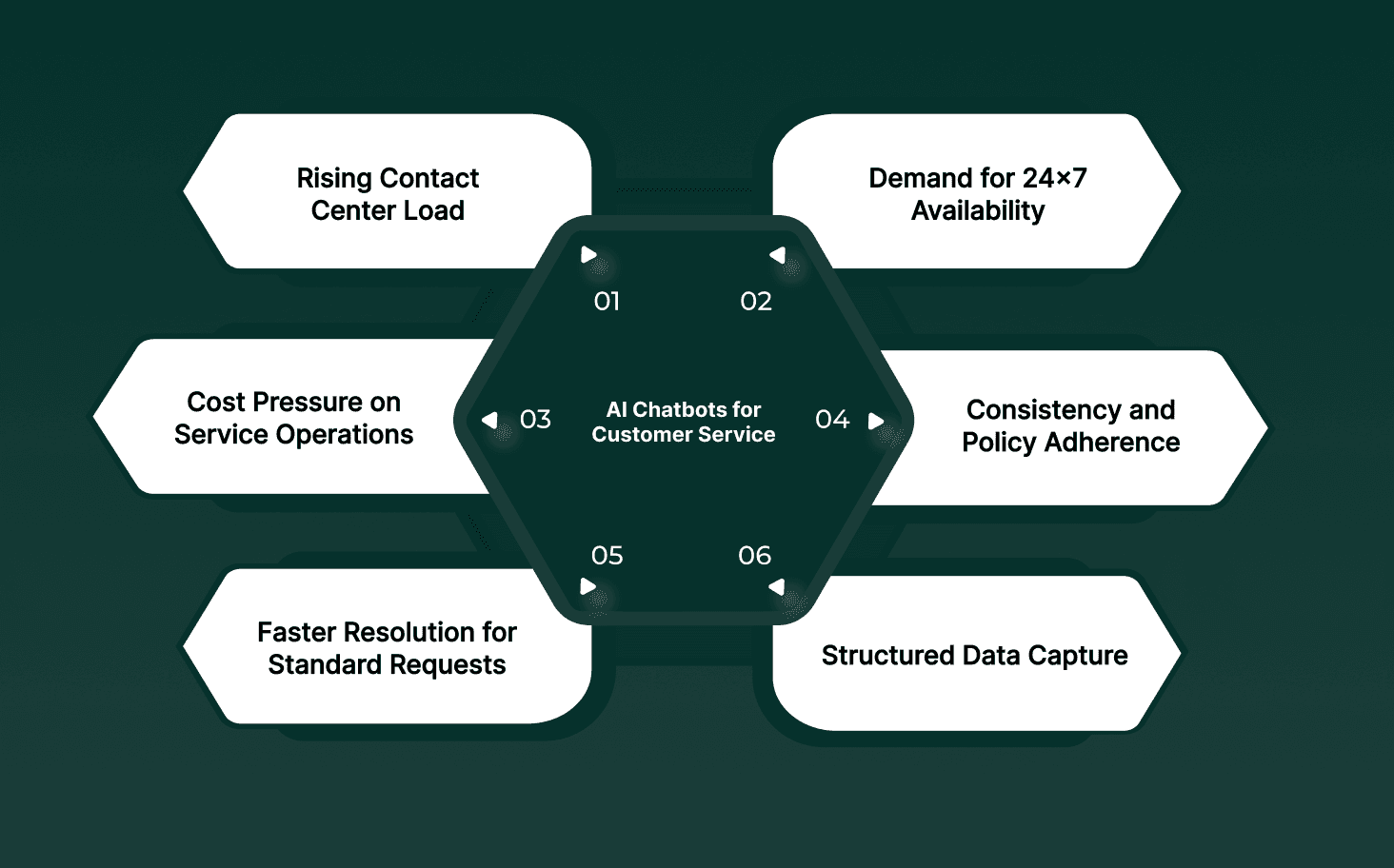

Why Banks Are Upgrading to AI Chatbots for Customer Service

Banks face sustained pressure from rising service volumes, regulatory scrutiny, and customer expectations for instant resolution across digital channels. AI chatbots are being adopted to handle high-frequency interactions with predictable accuracy while maintaining auditability and cost control.

Rising Contact Center Load: Mobile banking, UPI, and digital payments have increased inbound queries related to balances, failed transactions, KYC status, and card issues beyond what human teams can scale economically.

Demand for 24×7 Availability: Customers expect support outside branch hours. AI chatbots provide continuous coverage without staffing spikes during nights, weekends, or peak billing cycles.

Cost Pressure on Service Operations: Tier-1 banks handle millions of repetitive queries monthly. Chatbots reduce cost per interaction by offloading low-risk requests from live agents.

Consistency and Policy Adherence: AI chatbots respond using pre-approved flows tied to banking policies, reducing variance in responses and lowering compliance exposure.

Faster Resolution for Standard Requests: Tasks such as balance checks, statement downloads, card blocking, and loan status updates can be resolved in seconds without queue time.

Structured Data Capture: Chatbots collect intent, metadata, and conversation logs in a standardized format, supporting downstream analytics, QA reviews, and regulatory audits.

See how automation layers work together in modern banking operations and where conversational systems fit within broader workflows in 10 Ways RPA in Banking Improves Efficiency and Control

AI Chatbot Use Cases in Banking That Deliver Measurable ROI

AI chatbots are now a strategic tool for banks because they reduce operational costs, accelerate response times, and increase self-service containment rates. In 2025, 92% of North American banks use AI chatbots, and the global chatbot market in banking exceeds $2 billion.

The use cases below work because they connect directly to core banking systems, follow deterministic rules, and replace repetitive human labor without introducing advisory or compliance risk.

1. Account Balance and Transaction Queries

Balance checks and recent transaction requests consistently represent the highest share of inbound banking interactions across voice and digital channels.

Direct Core Banking Reads: Chatbots perform secure, read-only queries against ledger and transaction services with strict permission scopes.

Queue Elimination: Customers receive immediate responses instead of waiting through IVR trees or agent queues.

Agent Load Reduction: Human agents are freed from repetitive lookups and can focus on exception handling.

Example: A retail bank routes balance and last-five-transaction requests entirely through chatbots on mobile apps and IVR, reducing daily inbound call pressure during salary credit and billing cycles.

2. Card Blocking and Fraud Incident Reporting

Lost cards and suspected fraud require immediate action, making speed and accuracy more critical than conversational depth.

Authenticated Action Execution: After step-up verification, chatbots trigger card block APIs without agent involvement.

Structured Fraud Intake: Incident details are captured using predefined fields aligned with fraud investigation workflows.

After-Hours Coverage: Customers can secure accounts immediately without waiting for branch or call center availability.

Example: Banks deploy chatbots for card loss reporting overnight and on holidays, preventing delayed blocks that previously resulted in avoidable fraud exposure.

3. KYC Status Checks and Document Follow-Ups

KYC delays generate repeated customer contacts due to unclear status visibility rather than processing errors.

Workflow State Visibility: Chatbots surface the exact KYC stage from onboarding systems.

Precise Remediation Prompts: Customers receive clear instructions on missing or rejected documents.

Back-Office Deflection: Manual status lookups by operations teams are significantly reduced.

Example: A digital-first bank integrates its onboarding engine with chatbots to handle KYC queries, reducing repeat follow-ups during high-volume account opening campaigns.

4. Loan Eligibility Pre-Screening and Application Tracking

Loan-related queries consume both sales and service capacity when handled manually.

Rule-Bound Eligibility Logic: Chatbots apply predefined criteria without generating personalized advice.

Origination System Integration: Application status updates are pulled directly from LOS platforms.

Sales Qualification Control: Unqualified prospects are filtered before reaching relationship managers.

Example: Lenders use chatbots to pre-screen loan inquiries on websites and IVR, allowing sales teams to focus only on applicants meeting baseline criteria.

5. Payment Failures and Dispute Registration

UPI, card, and net banking failures create time-sensitive service spikes and repeat contacts if not handled correctly.

Failure Code Mapping: Chatbots classify errors using transaction response codes.

Automated Dispute Creation: Dispute tickets are opened with complete metadata on first contact.

Expectation Clarity: Customers receive defined resolution timelines aligned with banking policies.

Example: During peak shopping seasons, chatbots handle payment failure complaints end-to-end, preventing backlog buildup in contact centers.

6. Service Request Intake and Routing

Unstructured service requests increase handling time and routing errors.

Standardized Request Capture: Chatbots collect intent, urgency, and account context in a consistent format.

First-Time Correct Routing: Requests are assigned to the right queue without manual triage.

SLA Alignment: Customers receive accurate timelines based on request type.

Example: A mid-size bank replaces email-based service intake with chatbot-driven workflows, improving first-contact resolution and queue discipline.

See how Smallest.ai allows banks and enterprises to run real-time voice agents with controlled workflows, high concurrency, and enterprise-grade security by booking a demo today.

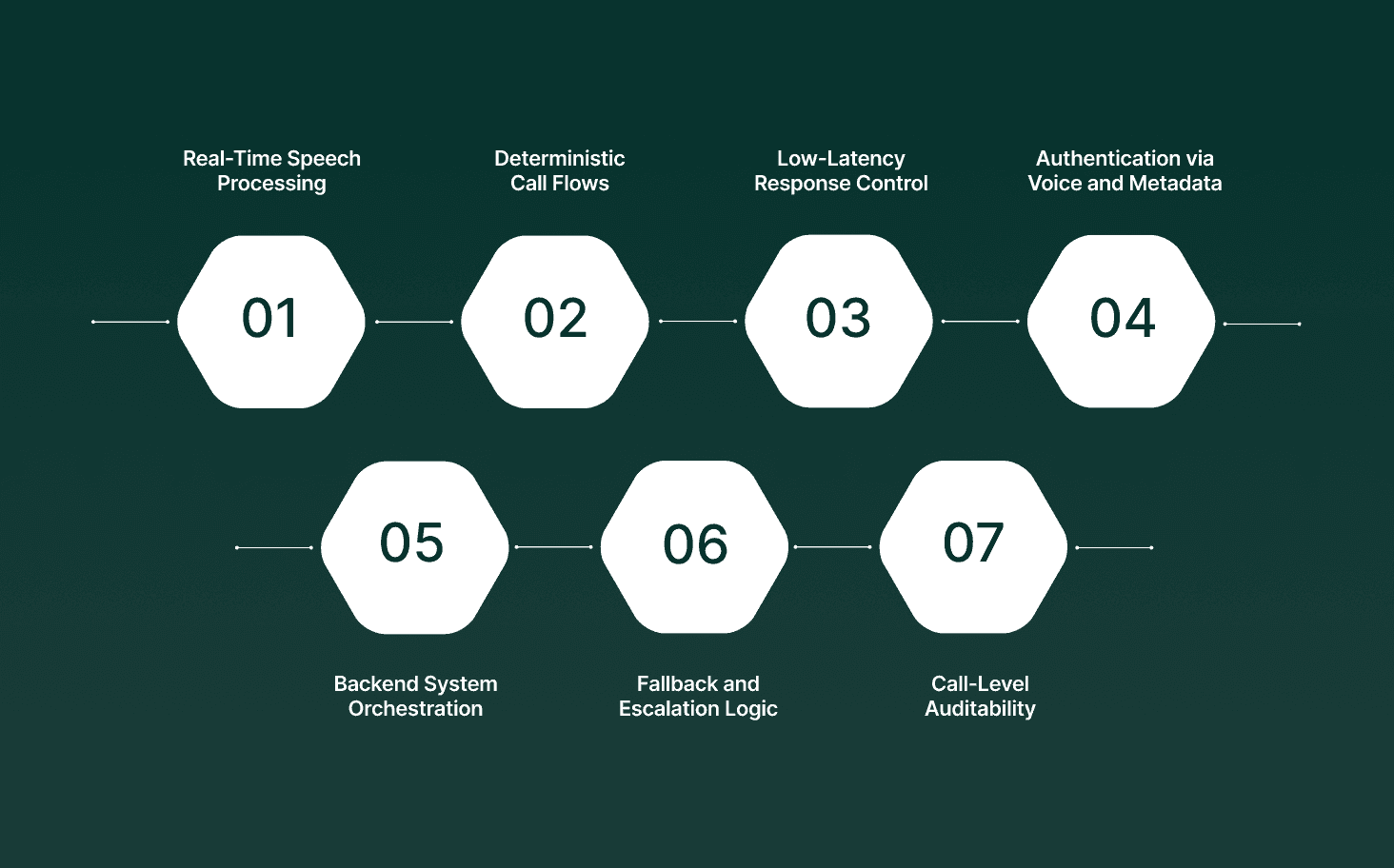

Using Voice AI Chatbots in Banking for Real-Time Customer Interactions

Voice AI chatbots operate directly on live calls, converting speech to structured intent, executing backend actions, and responding in natural language within tight latency thresholds. Banks deploy them to manage high-volume voice traffic while maintaining control over accuracy, security, and escalation.

Real-Time Speech Processing: Continuous speech-to-text and text-to-speech pipelines allow the agent to respond mid-conversation without waiting for call completion, keeping interactions fluid.

Deterministic Call Flows: Voice agents follow rule-bound conversation trees tied to banking SOPs, preventing off-policy responses during sensitive actions such as card blocking or account verification.

Low-Latency Response Control: Sub-second inference is required to avoid awkward pauses, interruptions, or talk-over, which directly affects customer trust on phone channels.

Authentication via Voice and Metadata: Voice AI integrates IVR inputs, device data, and caller history to support step-up verification before executing account-level actions.

Backend System Orchestration: Agents trigger CRM, core banking, ticketing, and fraud systems in real time, allowing end-to-end resolution without agent handoff.

Fallback and Escalation Logic: Calls transfer to human agents when confidence drops, policy thresholds are crossed, or emotional signals indicate frustration or risk.

Call-Level Auditability: Every utterance, action, and decision path is logged, supporting post-call review, dispute handling, and regulatory traceability.

Voice AI chatbots allow banks to handle live customer calls at scale while preserving response control, verification rigor, and escalation safety across real-time interactions.

Key Risks and Compliance Challenges of AI Chatbots in Banking

AI chatbots in banking operate within tightly regulated environments where errors can trigger financial loss, regulatory action, or customer harm. Banks must address technical, operational, and governance risks before deploying chatbots at scale.

Risk Area | Why It Matters in Banking | What Banks Must Control |

Data Privacy Exposure | Chatbots process PII, financial data, and credentials in real time, increasing breach impact | Encryption in transit and at rest, strict data retention rules, and field-level masking |

Regulatory Non-Compliance | Incorrect disclosures or advice can violate RBI, PCI DSS, GDPR, or sector-specific mandates | Policy-bound response templates, jurisdiction-aware logic, and compliance reviews |

Hallucinated Responses | Generative models may fabricate account details, fees, or eligibility criteria | Deterministic flows for sensitive intents, retrieval-only responses |

Authentication Weaknesses | Poor identity checks allow account takeover and fraud | Multi-step verification, voice biometrics, metadata-based risk scoring |

Audit and Traceability Gaps | Regulators require explainable decisions and replayable interactions | Full conversation logs, decision trees, action timestamps |

Model Drift Over Time | Changes in products or policies can cause outdated responses | Scheduled retraining, rule versioning, regression testing |

Escalation Failures | Missed handoffs can trap users in unresolved loops | Confidence thresholds, sentiment detection, forced human transfer |

Third-Party Dependency Risk | External models or APIs introduce vendor and availability exposure | On-prem or private deployments, SLA-backed inference controls |

Explore how production-grade voice AI is reshaping regulated banking conversations and see which platforms are built to handle real-time scale, compliance, and call complexity in Top AI voice agents for BFSI (Banking, Financial Services, and Insurance) in 2025?

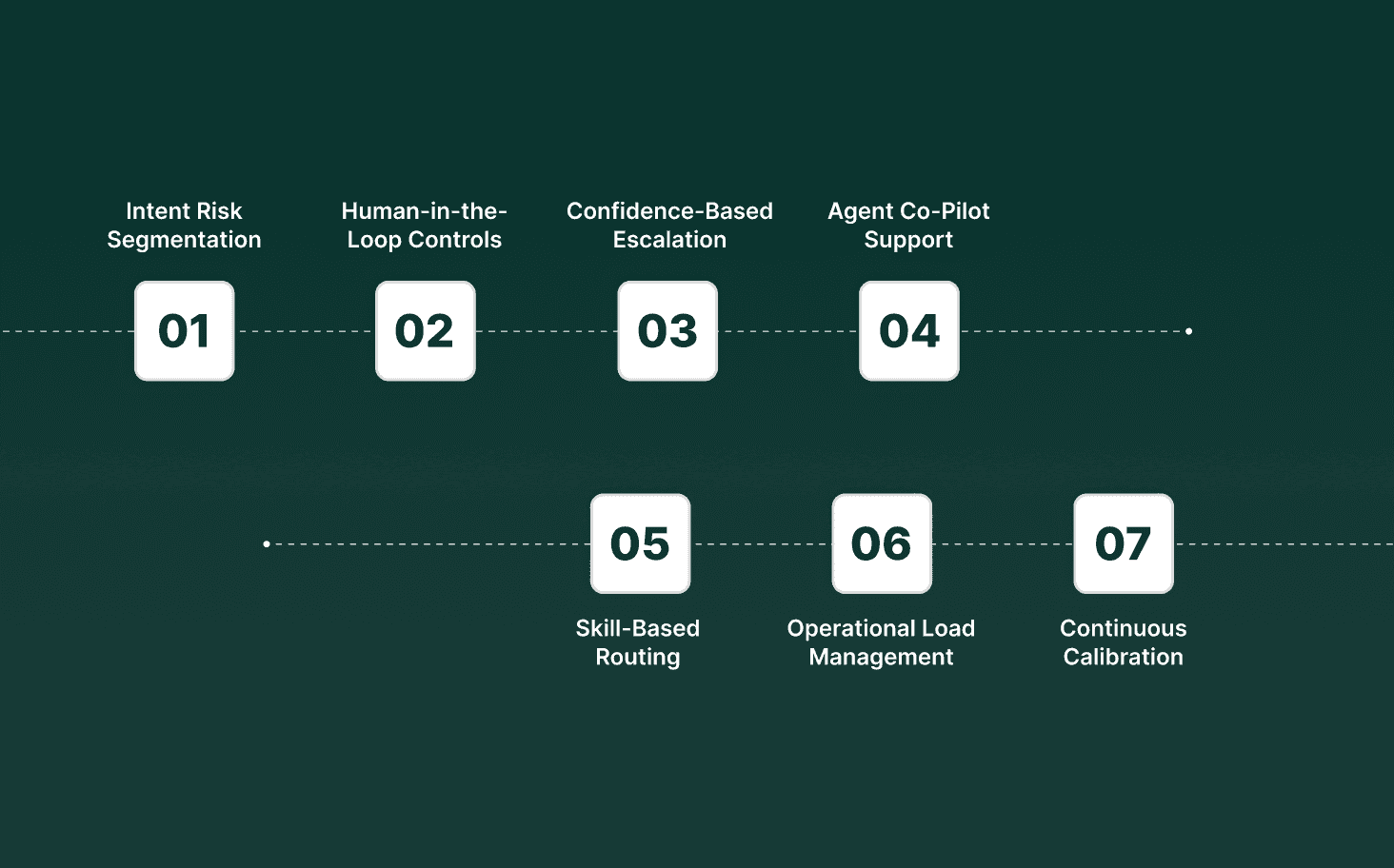

Balancing Human Expertise and AI Chatbots in Banking Operations

Banks achieve sustainable results with AI chatbots when automation is applied selectively, and human agents remain embedded in decision-critical paths. The balance depends on intent risk, financial impact, and regulatory sensitivity.

Intent Risk Segmentation: Low-risk, repeatable requests such as balance checks and statement access are automated, while high-risk intents route directly to trained agents.

Human-in-the-Loop Controls: Chatbots pause execution and request agent approval for actions involving limits, exceptions, or policy deviations.

Confidence-Based Escalation: Real-time confidence scoring determines when uncertainty crosses a defined threshold, triggering immediate handoff.

Agent Co-Pilot Support: AI provides agents with live summaries, recommended next actions, and compliance prompts during active calls or chats.

Skill-Based Routing: Escalated conversations are routed to agents trained in specific products, languages, or regulatory domains.

Operational Load Management: Chatbots absorb volume spikes during outages, payment failures, or campaigns, allowing agents to focus on resolution rather than triage.

Feedback and Continuous Calibration: Agent corrections and overrides feed back into rule updates and model refinement.

Banks that combine AI chatbots with structured human oversight gain scale without sacrificing judgment, compliance, or customer trust.

The Future of AI Chatbots in Banking and Customer Engagement

AI chatbots in banking are evolving from reactive support tools into operational systems that influence service design, risk detection, and customer relationship management. Future deployments prioritize control, explainability, and deep system coupling over conversational novelty.

Proactive Service Triggers: Chatbots initiate outreach based on transaction anomalies, payment failures, expiring cards, or missed EMIs rather than waiting for customer contact.

Unified Omnichannel Memory: Conversation context persists across voice, chat, mobile apps, and branches, allowing continuity without repeated verification.

Deeper Core Banking Integration: Chatbots execute multi-step workflows spanning ledgers, loan systems, CRM, and fraud engines without manual intervention.

Adaptive Compliance Logic: Regulatory rules are encoded as dynamic constraints that adjust responses by geography, product type, and customer segment.

Voice-First Customer Journeys: Voice AI handles complex, time-sensitive interactions where speed and clarity matter more than visual interfaces.

Real-Time Risk Signals: Behavioral cues from speech patterns, pauses, and escalation frequency feed into fraud and risk monitoring systems.

Measurable Outcome Ownership: Chatbots are evaluated on resolution rates, containment ratios, and regulatory incidents rather than engagement metrics.

The future of AI chatbots in banking centers on operational accountability, predictive service, and regulated autonomy rather than conversational polish.

How Smallest.ai Supports Production-Grade AI Chatbots in Banking

Banks deploying AI chatbots at scale need systems that behave predictably under live traffic, integrate cleanly with core infrastructure, and meet enterprise security requirements from day one. Smallest.ai is built specifically for real-time, high-volume voice and conversational workloads where latency, accuracy, and control matter.

Real-Time Voice Agents for Live Banking Calls: Smallest.ai runs continuous speech-to-text and text-to-speech during active calls, allowing chatbots to respond mid-conversation without pauses, interruptions, or turn-taking errors.

Enterprise-Ready Deployment Options: Banks can deploy Smallest.ai on cloud or on-premise infrastructure, retain control over inference, and run models on custom hardware to meet internal security and data residency requirements.

Deterministic, SOP-Driven Agent Behavior: Voice agents are designed to handle hundreds of edge cases using rule-bound workflows aligned with banking SOPs, reducing off-policy responses during sensitive interactions.

High-Concurrency Call Handling: The platform supports thousands of parallel calls per day, allowing banks to absorb traffic spikes during outages, payment failures, or peak transaction periods.

Precision with Numbers and Financial Data: Voice models are tuned for accurate handling of account numbers, credit cards, phone numbers, and acronyms, with controlled pacing and intonation.

Deep System Integration Surface: Python, Node.js, and REST APIs allow direct integration with telephony systems, CRMs, core banking platforms, ticketing tools, and analytics stacks.

Multilingual Banking Coverage: Support for 16+ global languages allows banks to serve customers across regions without duplicating agent infrastructure.

Enterprise Security and Compliance Controls: Built with SOC 2 Type II, HIPAA, PCI standards, and strict internal audit processes to support regulated banking environments.

For banks moving beyond chatbot pilots, Smallest.ai provides the real-time voice infrastructure, deployment flexibility, and operational control required to run AI chatbots as a core banking service layer rather than an experimental add-on.

Final Thoughts!

AI chatbots in banking have reached a point where the question is no longer whether they belong in production, but where they should operate and under what controls. Banks that see results treat chatbots as part of their service infrastructure, not as conversational layers sitting on top of legacy systems. The difference shows up in response quality, operational predictability, and how well automation holds up under real customer pressure.

As usage expands across voice and digital channels, success depends on execution discipline. Clear intent boundaries, real-time system access, controlled escalation, and audit-ready behavior separate dependable deployments from brittle ones. Banks that get this balance right reduce service strain without compromising trust or regulatory posture.

This is where platforms built for live, regulated environments matter. Smallest.ai provides real-time voice agents, enterprise-grade deployment options, and deterministic control designed for banking workloads that cannot afford guesswork.

Book a demo with Smallest.ai to see how production-grade voice AI can support secure, high-volume banking conversations.

How Do AI Chatbots in Banking Handle Policy Updates Without Causing Inconsistent Responses?

Can AI Chatbots in Banking Operate Safely Without Access to Full Customer Data?

How Do AI Chatbots in Banking Avoid Giving Regulated Financial Advice?

What Happens When AI Chatbots in Banking Misinterpret Customer Intent?

Are AI Chatbots in Banking Auditable for Regulatory Reviews?