Top 5 Open Banking and AI Use Cases Redefining Real-Time Financial Experiences

See how open banking and AI turn financial data into real-time actions. Discover use cases, voice AI impact, and what fintech teams must build next. Read more.

Every fintech team talks about open banking and AI, yet many still struggle to turn shared financial data into real-time customer experiences that actually feel responsive during live interactions. As open banking and AI adoption accelerate toward a market projected to reach $89.4 billion by 2033, product and engineering teams face growing pressure to move from static integrations to systems that react instantly to intent, voice, and context. Building connected financial journeys now means balancing speed, security, orchestration, and conversational interfaces without adding operational complexity.

For banking and fintech leaders, the challenge is less about accessing APIs and more about creating infrastructure that converts financial signals into actions while customers are still engaged. Teams want automation that feels natural, scalable, and compliant without breaking existing workflows or increasing latency.

In this guide, we take a look at how open banking and AI are reshaping financial architecture, where real-time voice fits into the stack, and what forward-looking teams should prioritize next.

Key Takeaways

AI Turns Open Banking Into Execution Systems: Open banking and AI shift platforms from data sharing to real-time workflows where intent triggers lending, servicing, and risk actions.

APIs Need Orchestration Layers: REST endpoints allow access, yet semantic models, event streaming, and execution layers allow AI to interpret context across fragmented banking systems.

Voice AI Becomes The Interaction Layer: Low-latency speech pipelines connect conversational intent to open banking APIs, allowing payments, onboarding, and support during live customer interactions.

AI-First Infrastructure Drives Advantage: Event-driven pipelines, microservices, and inference layers help banks execute decisions during interactions instead of relying on delayed batch processing.

Real-Time Voice Infrastructure Accelerates Adoption: Smallest AI supports full-duplex conversations, multilingual execution, and scalable voice agents that convert financial dialogue into transaction-ready experiences.

Why Open Banking and AI Are Finally Coming Together

Open banking exposed structured financial data through consent-driven APIs. AI matured into real-time execution engines. Together, they allow continuous financial workflows instead of static analytics dashboards.

Key technical shifts driving this convergence include:

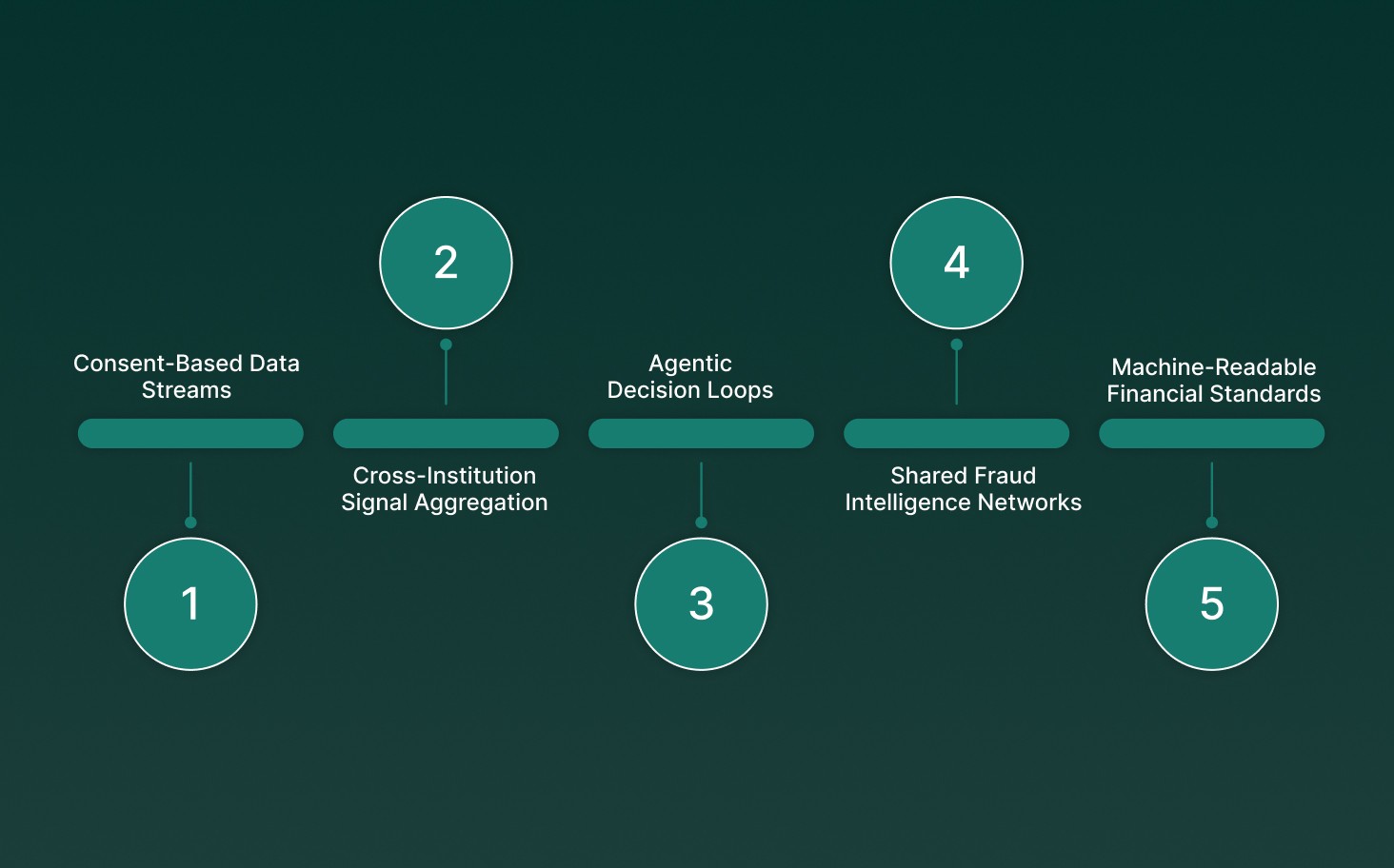

Consent-Based Data Streams: PSD2 APIs expose categorized transactions, balances, and payment initiation endpoints, allowing AI models to process live account events rather than batch exports.

Cross-Institution Signal Aggregation: Aggregators normalize merchant codes, timestamps, and payment rails data, giving AI models a unified behavioral context across multiple providers.

Agentic Decision Loops: AI agents combine event triggers with API permissions to execute actions like balance reallocation or credit limit updates without manual orchestration.

Shared Fraud Intelligence Networks: AI correlates device fingerprints, session anomalies, and transaction velocity signals across institutions to improve detection accuracy.

Machine-Readable Financial Standards: JSON schemas, ISO20022 mappings, and semantic taxonomies help AI interpret financial intent consistently across regions and regulatory frameworks.

Open banking delivers continuous financial signals, while AI adds autonomous interpretation, shifting finance toward responsive, execution-ready infrastructure.

Core AI Use Cases Emerging Across the Open Banking Ecosystem

Open banking APIs supply continuous financial signals. AI systems turn those signals into automated workflows across risk, servicing, compliance, and financial decisioning without relying on static rule engines.

Collaborative Fraud Detection and AML Intelligence

AI models analyze multi-bank payment streams, device telemetry, and behavioral anomalies to detect coordinated fraud patterns across institutions rather than reacting to isolated transaction alerts.

Operational gains from collaborative fraud intelligence include:

Cross-Account Pattern Correlation: AI clusters transaction velocity, merchant category deviations, and login anomalies across accounts to identify mule networks that traditional single-bank monitoring cannot detect.

Real-Time Risk Scoring Pipelines: Streaming models assign probabilistic risk scores during payment initiation using behavioral biometrics and API session metadata, reducing manual fraud review queues and alert fatigue.

Adaptive AML Graph Analysis: Graph neural networks map transaction relationships between entities, uncovering layered payment chains designed to bypass threshold-based compliance rules.

Hyper-Personalized Financial Servicing and Advisory

AI systems interpret normalized open banking data feeds to deliver context-aware financial guidance that adapts to spending behavior, liquidity signals, and account-level financial intent in real time.

Customer-facing advantages of AI-driven personalization include:

Intent-Aware Recommendation Engines: Models analyze categorized spending data and cash flow patterns to dynamically suggest refinancing, repayment scheduling, or liquidity optimization opportunities.

Contextual Portfolio Adjustments: AI integrates investment account APIs with real-time market signals, triggering allocation changes aligned with user-defined risk thresholds without requiring advisor intervention.

Lifecycle Event Detection: Transaction tagging models identify salary changes, subscription churn, or loan prepayments, allowing proactive financial nudges tied directly to evolving user behavior.

Agentic AI for Autonomous Money Management

Agentic systems combine API permissions with continuous monitoring to initiate financial actions autonomously, reducing the need for manual app navigation or repetitive user confirmations.

Automation-driven outcomes of agentic financial workflows include:

Automated Cash Flow Balancing: Agents monitor incoming and outgoing payments across linked accounts, redistributing funds to prevent overdrafts or optimize interest accrual without human oversight.

Dynamic Subscription Optimization: AI monitors recurring payment metadata and billing frequency, renegotiating or replacing services through partner APIs when better pricing or plans become available.

Event-Triggered Financial Transfers: Models monitor invoice schedules or payment deadlines, executing conditional transfers across banks when liquidity thresholds fall below predefined limits.

RegTech Automation and Compliance Intelligence

AI helps financial institutions manage regulatory complexity by transforming fragmented reporting data into machine-readable compliance workflows that update continuously instead of relying on periodic batch submissions.

Efficiency improvements driven by AI-powered RegTech include:

Automated Regulatory Data Mapping: AI models translate transaction schemas into regulatory formats aligned with jurisdictional reporting standards, reducing manual data transformation overhead.

Continuous Monitoring Dashboards: Machine learning models analyze API activity logs and transaction flows to flag compliance deviations before scheduled audits or reporting deadlines.

Explainable Compliance Scoring: Models generate traceable decision outputs using structured feature attribution, helping compliance teams justify automated actions during supervisory reviews.

AI-Powered Credit Decisioning and Financial Education

AI models extend traditional credit assessment by combining transactional insights with behavioral signals derived from open banking data streams, improving underwriting accuracy and consumer financial literacy.

Decisioning and education improvements allowed by AI include:

Behavioral Credit Modeling: Models evaluate spending consistency, income volatility, and savings behavior to generate alternative credit scores beyond legacy bureau data.

Real-Time Risk-Based Pricing: AI dynamically adjusts loan offers using live account balances and cash flow projections, reducing reliance on static underwriting snapshots.

Adaptive Financial Education Modules: Conversational AI generates contextual financial explanations tied to a user’s transaction history, turning passive insights into actionable learning moments.

Build real-time voice experiences with Smallest AI’s ultra-low latency speech stack, full-duplex conversations, multilingual agents, and on-prem deployment built for scalable, enterprise-grade financial workflows.

How Can Open Banking and AI Create Personalized Customer Experiences?

Open banking exposes real-time financial signals through consented APIs, while AI interprets context and adapts journeys across onboarding, lending, servicing, and retention in real time.

Personalized customer experiences in open banking depend on combining behavioral data, interaction history, and live inference to shape conversations, product flows, and service decisions dynamically:

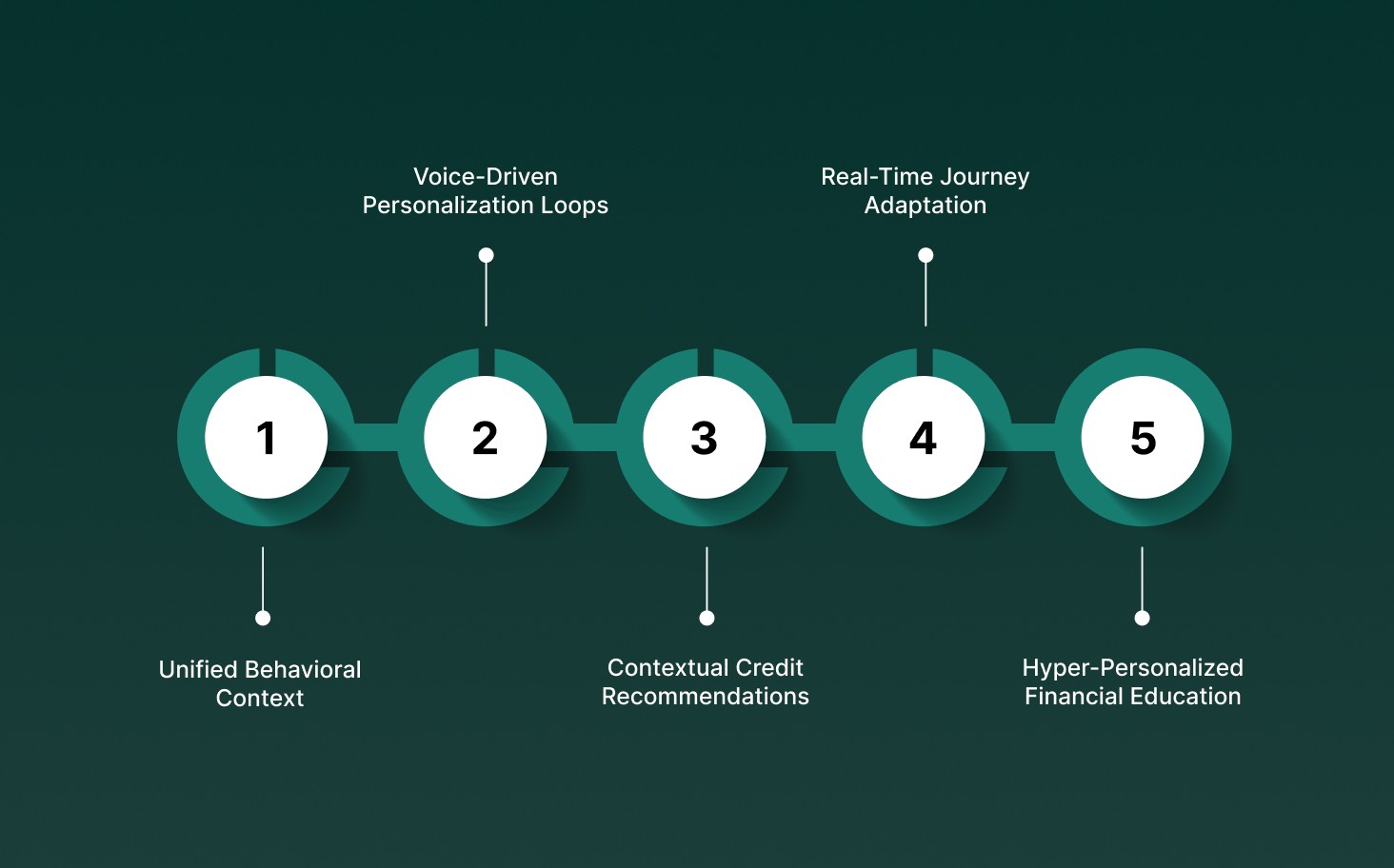

Unified Behavioral Context: Transaction categorization, merchant enrichment, and account aggregation help AI detect spending patterns like subscriptions, travel cycles, or income volatility signals.

Voice-Driven Personalization Loops: Speech recognition tied to customer profiles lets AI agents adjust tone, intent routing, and workflow execution during live voice interactions.

Contextual Credit Recommendations: Models evaluate cash-flow timing, recurring expenses, and income stability to surface lending options aligned with actual financial behavior instead of static bureau scores.

Real-Time Journey Adaptation: Event-driven triggers from payment APIs update onboarding steps, funding options, or support flows instantly without manual orchestration.

Hyper-Personalized Financial Education: Generative AI builds explainers using eligibility rules and transaction metadata, delivering guidance specific to each user’s financial activity.

Bring real-time voice and execution-ready AI into your lending workflows with infrastructure built for live financial conversations and scalable automation, and explore AI in SME Lending: What Is Actually Changing Day to Day?

Are APIs Enough to Power AI-Driven Banking Experiences?

APIs unlock data access, yet AI-driven banking needs semantic models, event orchestration, and execution layers. Without deeper architecture, APIs remain pipes rather than intelligence engines.

Key infrastructure layers allowing AI-native banking include:

AI-Driven Banking Layer | Why APIs Alone Are Not Enough |

Semantic Data Modeling | ISO20022 or BIAN-aligned taxonomies help AI interpret merchant data, payment intent, and account roles consistently across providers. |

Event-Driven Orchestration | Streaming via webhooks or Kafka lets AI react to balance changes, payment failures, and risk events without polling static API endpoints. |

Low-Latency Interaction Layer | Conversational inference and speech pipelines require sub-second processing, which traditional API gateways built for batch access struggle to deliver. |

Write-Capable Execution Frameworks | Autonomous workflows rely on payment initiation, mandate updates, and cross-provider actions secured through policy engines and permissioned write-access APIs. |

Legacy Abstraction Middleware | Microservices normalize core banking outputs, preventing inconsistent schemas from disrupting model training, orchestration logic, or real-time decision execution. |

Modern debt recovery demands real-time voice automation, compliant workflows, and scalable AI agents, discover what platforms are leading the shift in Top 10 AI Collection Tools for Debt Recovery in 2026.

Could Voice AI Become the Interface for Open Banking?

Voice AI combines speech recognition, intent modeling, and real-time API execution, turning financial conversations into actionable workflows instead of static app navigation or delayed customer service experiences.

Key voice capabilities shaping open banking interactions include:

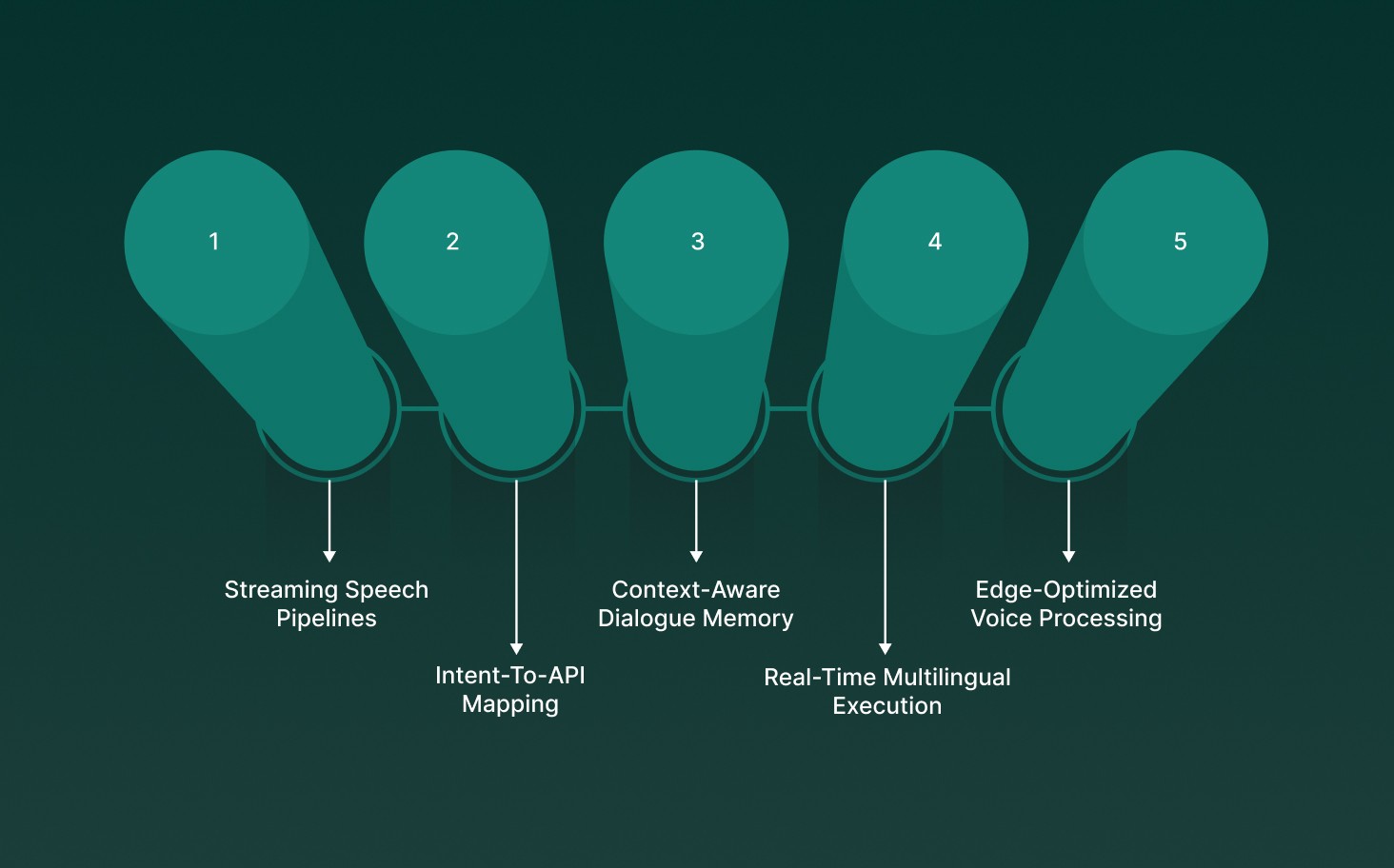

Streaming Speech Pipelines: Low-latency STT models such as Pulse STT process live audio streams, allowing AI systems to capture intent mid-sentence and trigger open banking actions without waiting for conversation completion.

Intent-To-API Mapping: NLP engines classify spoken commands into structured intents, converting phrases like “split rent” into payment initiation or account aggregation workflows across multiple providers.

Context-Aware Dialogue Memory: Persistent session memory tracks prior financial actions, letting voice agents maintain continuity across conversations, improving compliance logging, and reducing repetitive customer verification steps.

Real-Time Multilingual Execution: Voice AI supports multilingual speech synthesis and recognition, allowing open banking services to operate across regional markets without rebuilding separate interaction layers for each language.

Edge-Optimized Voice Processing: On-prem or edge deployments reduce latency and protect sensitive audio streams, aligning with banking security requirements while supporting continuous conversational interactions.

Voice AI can evolve into the primary open banking interface when speech infrastructure connects directly to financial workflows, turning spoken intent into secure, real-time transaction execution and personalized financial guidance.

What Banks Need to Build for AI-First Open Banking

AI-first open banking needs infrastructure built for speed, orchestration, and real-time execution. APIs alone do not allow automation without systems designed for continuous AI-driven decision flows.

Key technical foundations banks must prioritize to support AI-first open banking include:

AI-First Open Banking Foundation | What Banks Need To Build |

Event-Driven Data Pipelines | Stream transactions and consent signals instantly so AI reacts in real time instead of relying on batch processing cycles. |

Composable Microservices Stack | Break core banking into modular services so AI features connect without disrupting payments, onboarding, or servicing workflows. |

Low-Latency Inference Layers | Deploy lightweight models close to data sources to process intent, speech, and account activity without adding interaction delays. |

Unified Interaction Engine | Connect voice, chat, and APIs through orchestration logic that routes customer intent directly into banking workflows. |

Developer Testing Environments | Provide sandboxes, monitoring, and validation tooling, so teams can test AI behavior safely before launching production financial journeys. |

See how AI, automation, and real-time voice infrastructure are reshaping modern banking operations and customer engagement in Digital Transformation in Banking: Benefits, Tools & Use Cases.

Where Open Banking and AI Go From Here

Open banking is moving toward autonomous financial systems where AI interprets intent, triggers actions, and turns shared data into continuous operational intelligence.

The next phase focuses on broader data access, autonomous execution, and infrastructure built for real-time financial decision flows:

From Open Banking to Open Finance: AI pulls signals from investments, lending, insurance, and behavioral data to power predictive underwriting and lifecycle-driven financial journeys.

Rise of Autonomous Financial Agents: Agents monitor liquidity, trigger payment flows through APIs, and adjust financial strategies using live risk signals instead of static rule engines.

Collaborative Risk Intelligence Networks: Shared fraud telemetry and device signals help institutions detect coordinated threats across ecosystems rather than relying on isolated monitoring models.

Embedded Finance Expansion: Financial actions activate inside SaaS tools, marketplaces, and digital platforms through orchestration layers that connect contextual triggers with financial services.

Explainable Decision Infrastructure: Systems log consent, model inputs, and execution trails so regulators can audit automated outcomes without slowing real-time customer experiences.

Open banking is shifting from analytics dashboards to execution engines, where AI interprets signals continuously, and financial actions happen during live interactions rather than after workflows complete.

How Smallest AI Helps Build Real-Time Voice Experiences for Open Banking

Smallest AI allows banks to move from chatbot-style automation to full-duplex voice interactions, combining speech understanding, generation, and execution layers built for real-time financial conversations.

Key voice infrastructure capabilities include:

Hydra Full-Duplex Conversations: Multimodal architecture processes speech and text simultaneously, allowing users to interrupt, clarify, and transact naturally during live banking interactions without conversational lag.

Sub-300ms Voice Inference: Ultra-low latency response speeds keep financial conversations fluid, allowing real-time balance checks, onboarding flows, or payment confirmations without breaking conversational flow.

Enterprise Voice Agents At Scale: Agents handle thousands of concurrent calls, execute SOP-driven workflows, and manage multilingual interactions across lending, servicing, and support operations.

On-Prem Deployment Control: Banks run models on internal infrastructure, keeping financial data localized while maintaining fast speech generation and predictable performance for regulated environments.

Developer-Ready SDK Integration: Python, NodeJS, and REST APIs connect voice pipelines directly into telephony stacks, CRM systems, and open banking orchestration layers for production deployments.

Smallest AI brings execution speed to conversational finance, turning voice into a transaction layer where open banking actions happen instantly during live interactions instead of after digital form submissions.

Final Thoughts!

Open banking and AI are pushing financial products toward interaction-driven experiences where context matters as much as data itself. Teams that rethink how systems listen, respond, and execute during real moments will shape the next phase of digital finance. The shift is less about adding new tools and more about designing flows that react naturally to customer intent without slowing operations. Banks that focus on execution during conversations, not after them, will set the pace for what modern financial engagement looks like.

This is where platforms like Smallest AI help teams bring real-time voice into open banking journeys without rebuilding their entire stack. From low-latency speech infrastructure to scalable voice agents, the goal is to turn financial interactions into fast, natural conversations that actually move workflows forward.

If your team is building AI-native banking experiences, explore how Smallest AI can support real-time voice execution across onboarding, servicing, and customer engagement. Get in touch with us!

How is AI changing lesser-known open banking workflows beyond personalization?

Which open banking trends involve AI adoption at the infrastructure level?

Can open banking AI help banks manage interoperability challenges between standards?

Why are AI and open banking becoming important for real-time financial interactions instead of batch analytics?

AI allows intent recognition and live decision execution during interactions, allowing open banking systems to trigger payments, onboarding steps, or alerts instantly rather than processing events after delays.