9 Types of Predictive Analytics in Banking Used by Top Teams

Banks are racing toward predictive analytics in banking to improve outcomes. Explore the types and processes behind this shift before the next cycle hits.

Many banking teams face the same pressure. Calls, credit files, fraud alerts, and service queues move faster than internal systems can absorb. Decisions rely on scattered signals, and teams spend valuable time trying to connect patterns that should surface on their own.

Leaders who use voice AI, conversational AI, voice agents, and voice cloning already notice how interaction data carries intent and context that structured fields miss. Market growth reflects this shift as demand for these capabilities accelerates, with projections pointing to a CAGR of 19.2 percent from 2025 to 2033 and a value of USD 41.6 billion by 2033.

This is where predictive analytics in banking shows clear strength. When voice-driven cues merge with operational data, predictive analytics in banking gives teams earlier visibility into risk, intent change, repayment drift, fraud movement, and rising pressure in service lines.

In this guide, you will see 9 practical types used by top teams and the process behind each.

Key Takeaways

Voice-driven signals sharpen predictions: Banks that combine operational data with voice AI cues gain earlier visibility into repayment drift, fraud movement, churn intent, and service pressure.

Temporal rigor determines model reliability: Walk-forward validation, leakage control, and lifecycle-aligned cohorts prevent misleading accuracy and keep predictive systems stable across economic and product cycles.

Fraud and AML models rely on millisecond context: Real-time anomaly detection using device fingerprints, behavioral baselines, and ensemble scoring reduces false positives and catches coordinated activity earlier.

Conversational agents create automatic training labels: Outcomes from voice agents, resolutions, escalations, verifications, form fresh labels that accelerate retraining and increase predictive consistency across teams.

Unified customer histories improve downstream accuracy: Linking signals across voice, chat, email, CRM, and product systems strengthens features for credit, service, and compliance predictions.

Why Banks Use Predictive Analytics For Better Decisions

Predictive analytics in banking gives teams an early view of patterns that shape lending, fraud control, service planning, and capital allocation. Banks rely on it to act with speed and confidence across functions that carry financial and regulatory risk.

The value comes from faster visibility into shifts in customer behavior, credit signals, and operational strain points that would otherwise sit buried in daily activity.

Credit and repayment risk signals: Models track changes in payment rhythm, income patterns, and account activity to surface early delinquency indicators across portfolios.

Cross-channel fraud and anomaly detection: Patterns from transactions, device behavior, and voice transcripts connect in real time to flag suspicious activity before losses escalate.

Liquidity and deposit flow forecasting: Inflow and outflow models spot shifts in customer movement so treasury teams plan cash positions with clearer forward visibility.

Customer movement and product intent scoring: Behavioral cues, product usage, and engagement trends rank accounts for retention, cross-sell, or proactive outreach.

Contact center triage and portfolio stress alerts: Predictions steer sensitive calls to skilled staff, automate routine cases, and surface regional or product-level stress before it spreads.

If you’re mapping out where voice data can strengthen your predictive models, you’ll find a deeper breakdown here: Voice AI for Banks & Financial Services: Use Cases, Architecture & Best Practices

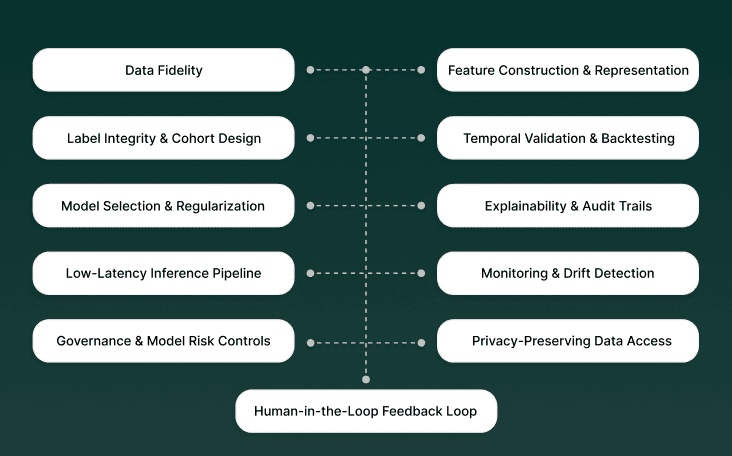

Core Elements Behind High-Accuracy Predictive Analytics In Banking

Predictive analytics in banking wins when teams treat models as live decision systems, not static reports. That requires strict data contracts, temporal rigor, measurable action links, and governance that ties model output to clear operational steps.

Data fidelity: Raw feeds must have lineage, completeness checks, timestamp accuracy, and reconciliation with accounting systems.

Feature construction and representation: Use domain-aware features like rolling cashflow ratios, behavioral embeddings, and derived event rates with fixed time windows.

Label integrity and cohort design: Define outcomes against business calendars, avoid label leakage, and create cohorts aligned to product lifecycles.

Temporal validation and backtesting: Backtest on contiguous time blocks, run walk-forward tests, and report performance decay by cohort and month.

Model selection and regularization: Prefer parsimony; choose models that balance generalization and interpretability for auditability.

Explainability and audit trails: Produce feature attributions, counterfactual checks, and human-readable rationale for high-impact decisions.

Low-latency inference pipeline: Separate batch scoring from online microservices with cached features and fast model lookups.

Monitoring and drift detection: Track label drift, feature distribution shifts, and business-metric divergence with automated alerts.

Governance and model risk controls: Maintain model inventory, versioned approvals, validation reports, and input/output access logs.

Privacy-preserving data access: Use tokenization, secure enclaves, and differential privacy where regulation mandates restricted data use.

Human-in-the-loop feedback loop: Route edge cases to specialists; capture overrides as labeled examples for retraining and calibration.

With the core elements in place, the next step is understanding where these models create the most value. Different banking teams apply predictive systems in distinct ways.

Predictive Analytics In Banking Methods And The Value They Add

Banking teams lean on different predictive methods depending on the problem in front of them. Credit teams watch for early repayment drift, fraud teams need signals that surface in milliseconds, and service or AML teams rely on patterns that cut across channels.

Each method solves a different pressure point, and together they help banks act earlier with clearer context. Below is how top teams use these approaches in daily work.

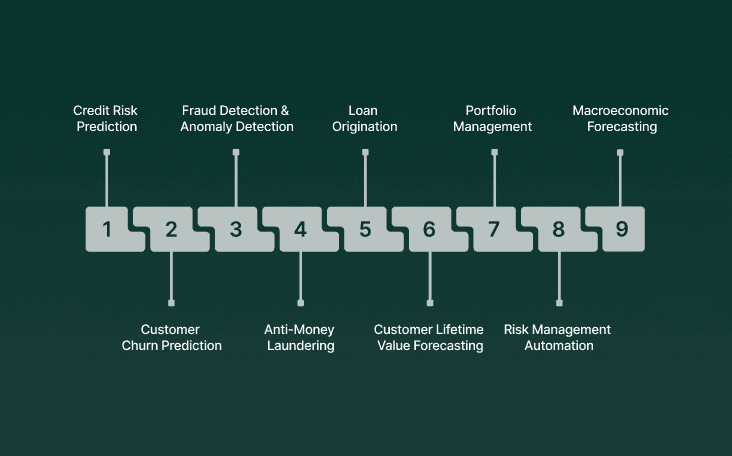

1. Credit risk prediction and default modeling

Traditional credit scoring treats risk as static. Predictive analytics in banking replaces this with a live probability model that updates as borrower behavior, product seasoning, and economic factors shift.

Hybrid model stacks (deep learning for feature extraction plus ensemble methods for ranking) capture non-linear interactions that older techniques miss, giving banks earlier and more granular visibility into repayment behavior.

Early default indicator detection: Neural networks spot subtle behavioral drift, such as slower repayment rhythm, abnormal spending clusters, or rapid credit line usage spikes.

Probability of default refinement: Feature extractors feed ensemble models, so borderline cases are separated from stable profiles with greater clarity.

Portfolio-level risk aggregation: Default probabilities roll up to portfolio dashboards, exposing sector clusters, emerging weak pockets, and stress exposure across product groups.

2. Customer churn prediction and retention targeting

Churn in banking affects deposits, lending, and advisory revenue at the same time. Predictive analytics banking teams rely on separating short-term inactivity from true disengagement so retention efforts land before the customer exits across products.

Behavioral cluster-based churn segmentation: Deep models group clients based on activity rhythm, product breadth, and financial habits, so each segment gets a tuned churn signal.

Soft-churn and hard-churn dual modeling: Soft-churn models focus on early disengagement patterns; hard-churn models track decisive exit behavior.

Intervention prescription scoring: Secondary models estimate which outreach type or benefit has the highest recovery probability for each at-risk segment.

3. Fraud detection and anomaly detection at scale

Fraud patterns shift as attackers probe new channels. Banking predictive analytics uses anomaly models that learn individual behavior envelopes and detect deviations in milliseconds, reducing both false positives and missed events.

Contextual baseline learning: Models build personal profiles combining transaction rhythm, device fingerprints, usual merchant categories, region patterns, and time-of-day activity.

Ensemble anomaly detection: Multiple models run in parallel: isolation forests for speed, autoencoders for complex deviations, and cluster models for peer context.

Real-time millisecond scoring: Streaming infrastructure pushes each event through deployed models so anomalies surface before transaction completion.

4. Anti-money laundering and transaction monitoring

Legacy AML systems flood analysts with alerts due to rigid rules. Predictive analytics in banking sector teams use dynamic scoring systems that track movement patterns, structural flow anomalies, and correlated activity across accounts.

Dynamic risk scoring: Risk levels adapt with new transfers, counterparties, and region shifts instead of staying fixed.

Behavioral pattern analysis: Models learn each customer’s baseline structure, transfer size ranges, typical counterparties, and channel patterns, and highlight deviations tied to laundering tactics or legitimate changes.

Cross-behavior correlation detection: Systems detect patterns across multiple clients that resemble coordinated activity, a hallmark of mule networks and layering operations.

5. Loan origination and approval automation

Predictive analytics for banking and financial services is central to underwriting modernization. Models rank applicant risk with greater precision, reduce manual review cycles, and support consistent decisions across branches and digital channels.

Feature selection optimization: Feature selection highlights income stability, repayment history patterns, cashflow volatility, collateral quality, and other strong predictors.

Decision tree explainability: Tree-based models produce clear rationale paths that meet audit requirements and support transparent approval communication.

Pricing integration: Risk predictions feed pricing engines so loan terms reflect expected performance and protect portfolio strength.

6. Customer lifetime value forecasting and retention strategy

CLV models help banks forecast long-term value across deposits, credit, investments, and channel activity. Predictive systems combine behavioral sequences with product-level economics to allocate retention and acquisition spend more accurately.

Sequential pattern modeling with behavioral clustering: Sequence models read transaction order, seasonality, and cross-product activity while clusters reveal groups with similar economic potential.

Discounted cash flow forecasting: Predicted future revenue accounts for churn probability, product upgrade likelihood, and spending rhythm across channels.

Service-level tier optimization: Banks use CLV estimates to adjust service levels, giving high-value segments more personalized human support and others automated channels.

If you want real conversational data to feed your predictive models with clarity and low latency, our voice AI platform can show real impact. You can book a demo.

7. Portfolio management and trading strategy support

Predictive models support treasury and investment desks by scanning market signals, volatility patterns, liquidity stress indicators, and macro shifts. Machine learning identifies patterns that traditional diversification frameworks miss.

Dynamic asset reallocation: Models adjust allocation when market and volatility patterns suggest a regime change.

Volatility prediction for risk control: Neural networks project volatility regimes, guiding pre-emptive position sizing.

Reinforcement learning strategy adaptation: Agents test thousands of scenarios in simulation and refine trading strategies in live environments.

8. Regulatory compliance and risk management automation

Compliance teams face extensive reporting and control requirements. Predictive analytics banking platforms help by automating mapping, testing, and exception spotting across controls and policies.

Automated compliance gap detection: Models read internal controls and regulatory text to surface mismatches and weak control points.

Regulatory update tracking: Systems monitor regulatory bulletins and map required changes to controls and documentation.

Continuous control performance checks: Predictive scores indicate when controls drift from intended performance, prompting early remediation.

9. Macroeconomic forecasting and scenario planning

Banks require forward visibility into interest rate moves, inflation patterns, liquidity stress, and credit conditions. Predictive models fuse econometric signals with machine-learning insights to detect early turning points.

Stress scenario modeling: Generative models simulate rare events to test capital and liquidity strength.

Leading indicator signal fusion: Models combine rates data, credit spreads, options volatility, fund flow trends, and sector signals to detect future macro shifts without relying on lagging indicators.

Portfolio resilience analysis: Portfolio simulations show how loans, deposits, and securities respond under stress paths so teams can adjust before conditions worsen.

Knowing the types is one piece; applying them inside daily workflows is another. A clear process helps banks translate model output into consistent action.

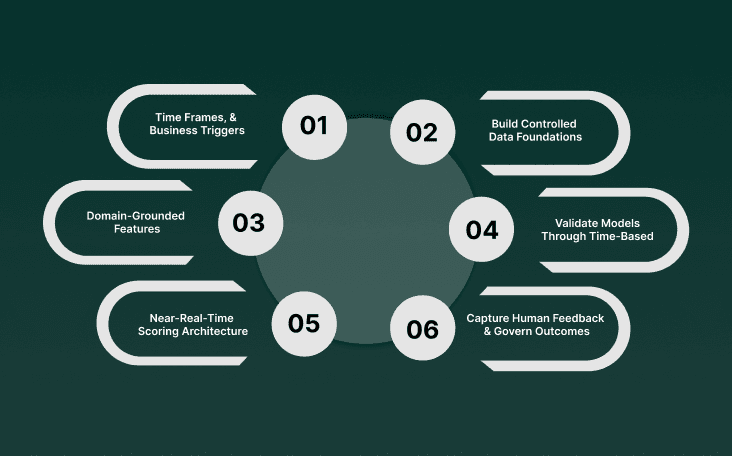

Step-by-Step Flow For Applying Predictive Analytics In Banking

Predictive analytics in banking works best when banks treat the entire pipeline as a governed decision system. Each stage must maintain temporal discipline, data reliability, operational clarity, and auditable logic so downstream teams can act with confidence.

Define outcomes, time frames, and business triggers: Set the decision the model supports, the prediction window, the observation window, and the exact action teams take when a score crosses a threshold.

Build controlled data foundations: Create data contracts for every feed, validate freshness and completeness, and resolve lineage to prevent drift in features tied to credit, fraud, AML, or operations.

Construct labels, cohorts, and domain-grounded features: Develop leakage-free labels, design cohorts that reflect product lifecycles, and engineer features such as rolling ratios, event-rate trends, and behavioral embeddings.

Select and validate models through time-based testing: Use algorithms that offer strong predictive power with audit-friendly explanations, then validate with walk-forward tests, stress-period segments, and calibration checks.

Deploy with real-time or near-real-time scoring architecture: Separate batch recompute pipelines from online scoring paths; store precomputed features in low-latency retrieval layers to support millisecond or sub-second decisions.

Monitor drift, capture human feedback, and govern outcomes: Track feature shifts, label drift, and KPI movement; record analyst overrides for retraining; maintain versioned audit trails and runbooks that bind predictions to actions.

Even the strongest process must operate within regulatory boundaries. These rules influence how models are built, tested, deployed, and reviewed.

Conversational AI Agent Support For Predictive Analytics In Banking

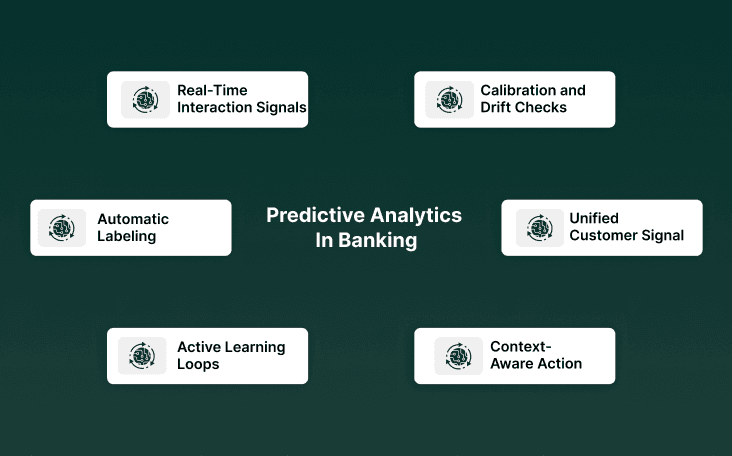

Conversational AI agents strengthen predictive analytics in banking by turning live customer interactions into structured, high-value data streams while enforcing model-driven actions in real time. They support both upstream feature creation and downstream decision execution, giving banks continuous feedback that strengthens every retrain cycle.

Real-time interaction signals and transcript features: Agents convert voice or chat sessions into structured events such as intent shifts, sentiment change, escalation clues, and entity timelines.

Automatic labeling from outcomes: Agent-handled sessions, resolutions, and follow-up actions act as fresh training labels, reducing manual annotation and improving model refresh speed.

Active learning loops for uncertain cases: Ambiguous interactions route to human staff, and the resolved cases return as labeled examples that sharpen model boundaries.

Context-aware action enforcement: Agents apply model outputs during interactions, adjusting flows or triggering verification when risk or priority scores require human review.

Unified customer signal stitching: Agents merge identifiers across voice, chat, and email so models receive a complete cross-channel feature set.

Feedback signals for calibration and drift checks: Conversion results, dispute outcomes, repayment behavior, and escalation events feed calibration pipelines and surface feature or label drift.

With these inputs, predictive systems stay current and grounded in the interactions that shape daily credit, fraud, and service outcomes.

How Smallest.ai Supports Predictive Analytics In Banking

Smallest.ai strengthens predictive analytics in banking by turning real-time conversations into structured signals, allowing faster decision cycles across credit, fraud, service, and compliance workflows. Its voice agent stack gives banks high-quality behavioral data, low-latency inference pathways, and continuous feedback needed for precise models and operational consistency.

Real-time conversational signal capture: Voice agents convert live calls into structured cues such as intent shifts, hesitation points, clarification patterns, and entity references that enrich feature sets.

High-fidelity transcription with enterprise accuracy: Speech-to-text pipelines extract phrases, event markers, and sentiment shifts with tight timestamps suitable for credit, fraud, and service prediction tasks.

Low-latency TTS and agentic responses: Lightning-grade models respond within sub-second windows, allowing predictive scores to guide call flow while maintaining natural conversation rhythm.

Outcome labeling from agent workflows: Resolutions, callbacks, verifications, and escalations create labeled examples that feed retraining cycles without heavy manual review.

Cross-channel identity stitching: Voice, chat, email, and CRM cues are linked to form unified customer histories that support richer predictive features.

Secure deployment for regulated workloads: SOC 2 Type 2, HIPAA, PCI, and on-prem options support strict data residency and governance requirements inside banks.

Together, these capabilities give banks a sharper flow of signals that strengthen predictive output where timing and accuracy matter most.

Conclusion

Predictive analytics in banking grows stronger when banks feed it with signals that reflect real interactions, not only structured fields. Voice-driven cues add clarity on intent, behavior shifts, and rising pressure across credit, fraud, and service lines.

Smallest.ai supports this by using voice AI, conversational AI, voice agents, and voice cloning to turn every call into reliable, time-stamped data. These signals strengthen features, speed up feedback loops, and keep model output closely tied to what customers express in live conversations.

If you want to see how these capabilities plug into your predictive workflows and contact center systems, book a demo.

FAQs About Predictive Analytics in Banking

1. What internal signals do teams often miss when deploying predictive analytics in banking?

Teams overlook conversational cues, case-handling events, and operator overrides. These signals strengthen feature sets for credit, fraud, and service scoring.

2. How does the predictive analytics banking industry measure long-term model stability?

Banks track month-to-month calibration, drift in feature distributions, and shifts in cohort behavior tied to product cycles or macro conditions.

3. Why do predictive analytics for banking & financial services require strict temporal framing?

Time windows must match real workflows. Misaligned observation or prediction windows lead to leakage and weak probability reliability.

4. What role do voice interactions play in bank predictive analytics pipelines?

Voice sessions supply labeled events, customer intent markers, and escalation clues that enrich models across the predictive analytics in banking sector.

5. How does the predictive analytics in banking market view on-prem and hybrid deployment choices?

Infrastructure choices depend on latency needs, data residency rules, and model governance. Many banks adopt hybrid setups to balance control and scale.