AI voice agents for collections and payments: automate outreach, stay TCPA/FDCPA compliant, reduce latency issues, and run a hybrid AI-human model.

AI voice agents for collections and payments are automated conversational systems that combine speech synthesis, speech recognition, and language understanding to reach customers about outstanding balances, set up payment arrangements, and run transactions without a human agent on the call. Done properly, they can run at high volume, 24/7, while staying inside regulatory lines like the TCPA and FDCPA.

Financial services has historically leaned on outbound call centers to recover debt and nudge customers before payments go late. That approach is costly, uneven in execution, and harder to staff every year. AI voice agents change the shape of the workflow: not by erasing humans from the process, but by becoming the first layer of outreach that is always available, consistently delivered, and built to scale.

Why Collections and Payments Is a Natural Fit for Voice AI

Most collections calls run on familiar rails. Identity check, balance disclosure, payment options, outcome logging, repeat. That repeatability is where voice automation shines. A meaningful slice of that momentum is tied to automating collections and payments work that used to require a seat in a call center.

Scale is only half the story; consistency is the other. Human agents inevitably vary, in tone, in script adherence, in how they respond when a call turns tense. A well-scoped AI voice agent delivers the same measured, compliant interaction on call ten thousand as it does on call one. In collections, where one stray line can create regulatory exposure, that uniformity is worth real money. For more detail on the banking angle, see AI voice agents for debt collection in banking.

How AI Voice Agents Actually Work in a Collections Context

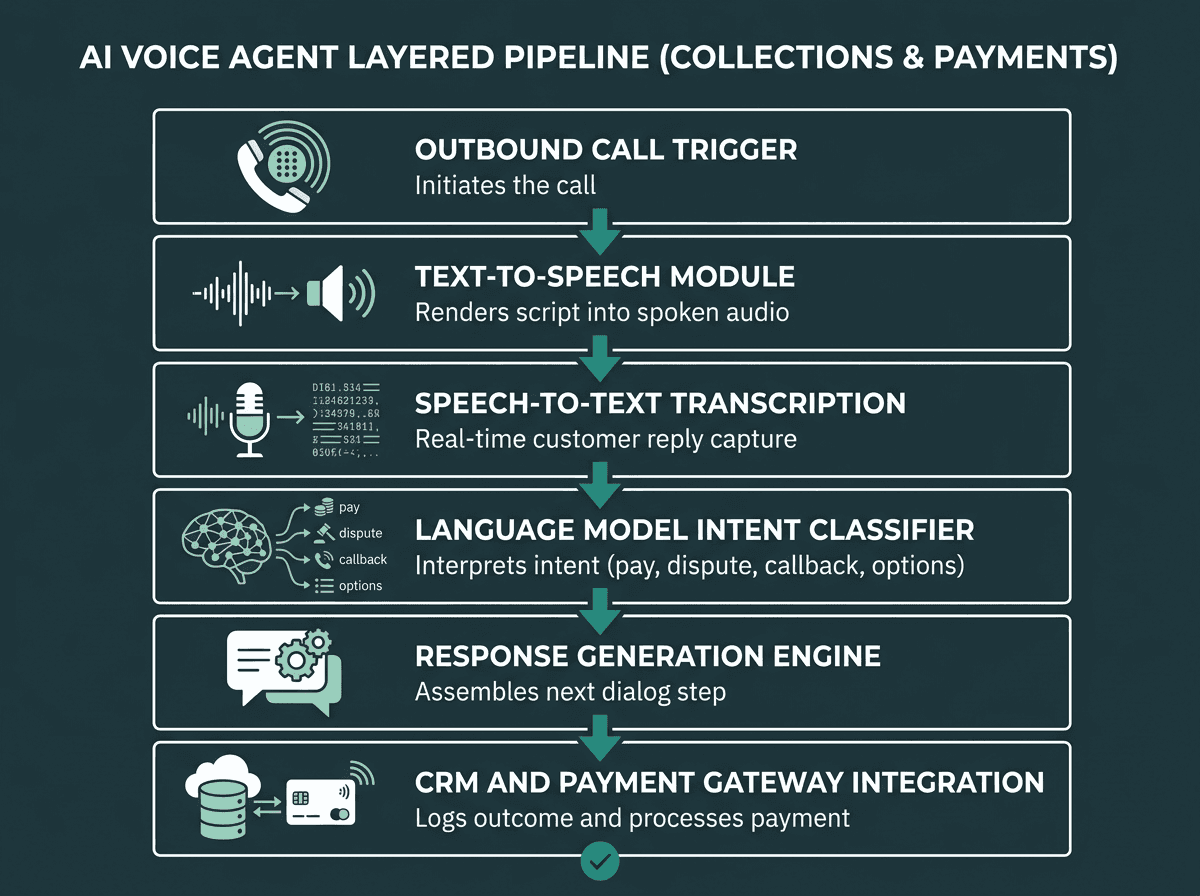

A collections voice agent is not a phone tree with nicer audio. It is a pipeline: multiple specialized components handing work to the next one in real time. The system kicks off an outbound call, then a text-to-speech engine renders the script (or a dynamically assembled prompt) into spoken audio. When the customer answers, speech-to-text transcribes the reply as it comes in. A language model interprets intent, agreeing to pay, disputing the debt, asking for a callback, requesting options, and chooses the next step in the dialog.

The plumbing matters, and latency is where many deployments live or die. Lower latency generally creates more natural and responsive voice interactions, while longer pauses make conversations feel less fluid. Systems stitched together from separate, unoptimized models often miss that bar, which is why they come across as robotic and irritating. Platforms built specifically for real-time voice tend to manage the handoffs more cleanly. The post on AI voice agent architecture and safety guardrails lays out the model stack and the guardrails that keep it reliable.

Six-layer pipeline showing how an AI voice agent handles collections calls end to end.

The Compliance Layer: What Makes or Breaks a Collections Voice Agent

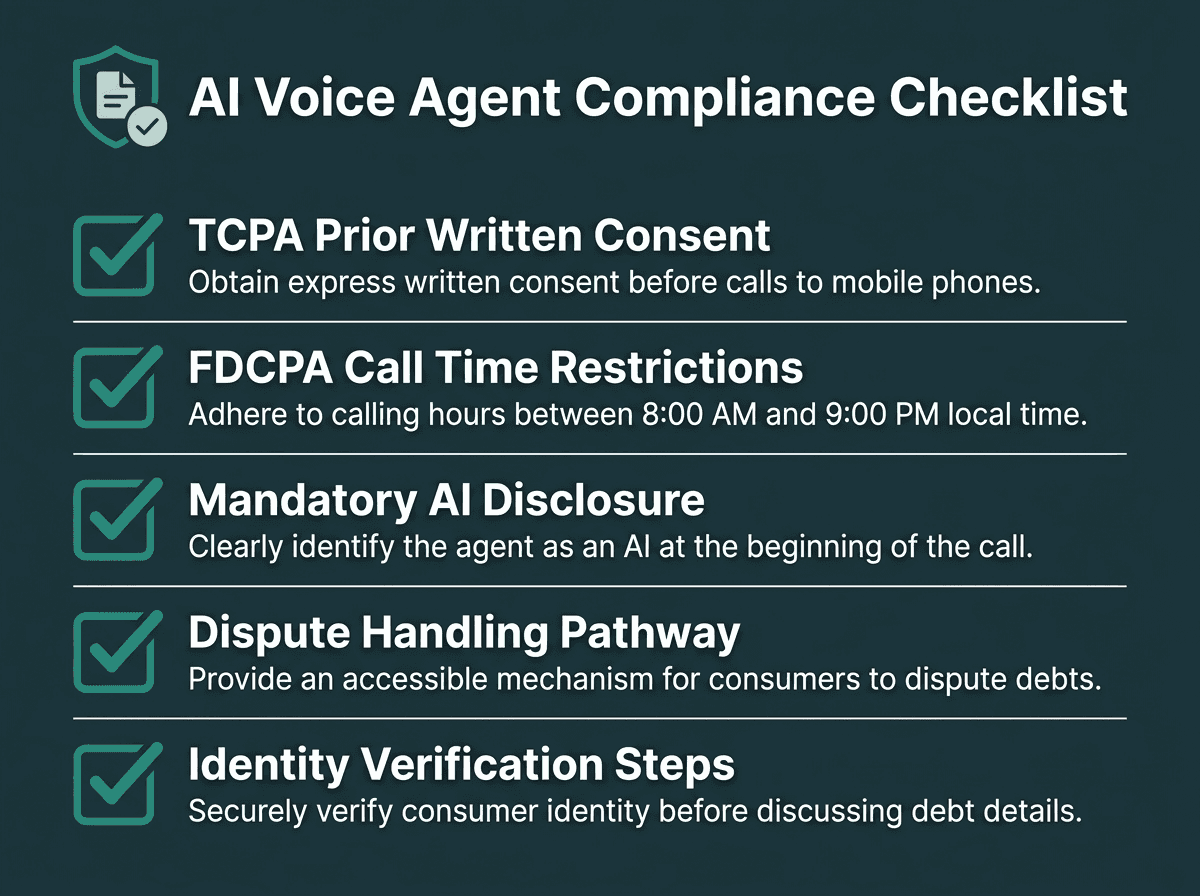

Collections is one of the most regulated communication environments you can put a voice system into. In the United States, the Fair Debt Collection Practices Act (FDCPA) sets rules for what collectors can say, when they can call, and how disputes are handled. Then there is the Telephone Consumer Protection Act (TCPA): in February 2024, the U.S. Federal Communications Commission ruled that AI-generated voices count as an artificial or prerecorded voice under the TCPA, which means prior express written consent is required before placing AI-generated calls to consumers. (Federal Communications Commission, 2024)

So compliance cannot be bolted on after the demo. It has to be part of the design: consent capture and storage, call-time windows, mandatory disclosure that the caller is automated, and straightforward ways for a consumer to opt out or ask for a human. The FDCPA guidelines for voice AI in debt collection break down how those requirements show up in call flows and agent behavior.

Identity verification sits right next to compliance because the risk is the same: disclose the wrong thing to the wrong person and you have a problem. Before any balance details are shared, the agent needs to confirm it is speaking with the account holder. That can be done with knowledge-based checks such as the last four digits of a social security number or a billing zip code. Some deployments go further with secure speaker verification with voice biometrics, matching the caller to the unique acoustic signature of their voice.

Every AI voice agent in collections must address these five regulatory requirements before deployment.

Types of Interactions AI Voice Agents Handle in Payments and Collections

Collections and payments work is not one monolithic "call type." It is a mix of repeatable interactions and genuinely messy edge cases. Voice agents perform best when you define that taxonomy up front and aim automation at the parts that are stable. Here is what that usually looks like:

Common interaction types handled by AI voice agents in this space:

Payment reminders: Outbound calls that flag upcoming or overdue balances, with the option to pay immediately via IVR or switch to a secure payment link sent by SMS.

Promise-to-pay capture: The agent offers payment options, the customer chooses one, and the commitment is written back into the CRM without human touch.

Dispute intake: When a customer disputes a charge, the agent gathers the details, logs the dispute, and kicks off the workflow for human review.

Settlement offers: For late-stage accounts, the agent can present pre-approved settlement amounts and record acceptance, reducing the amount of live-agent negotiation required.

Payment confirmation: Inbound calls where customers verify that a payment went through or ask for a receipt, handled end-to-end without queue time.

Escalation routing: When the conversation crosses the agent's boundaries, a legal threat, a complex dispute, the system transfers to a live agent and carries over full context.

This range is why collections teams adopt voice agents for more than cost savings. Coverage matters. A human team working business hours will never match the contact rate of a system that can run 24 hours a day across time zones, weekends included. For a wider scan of where conversational systems show up in finance, conversational AI banking use cases maps the broader set of workflows.

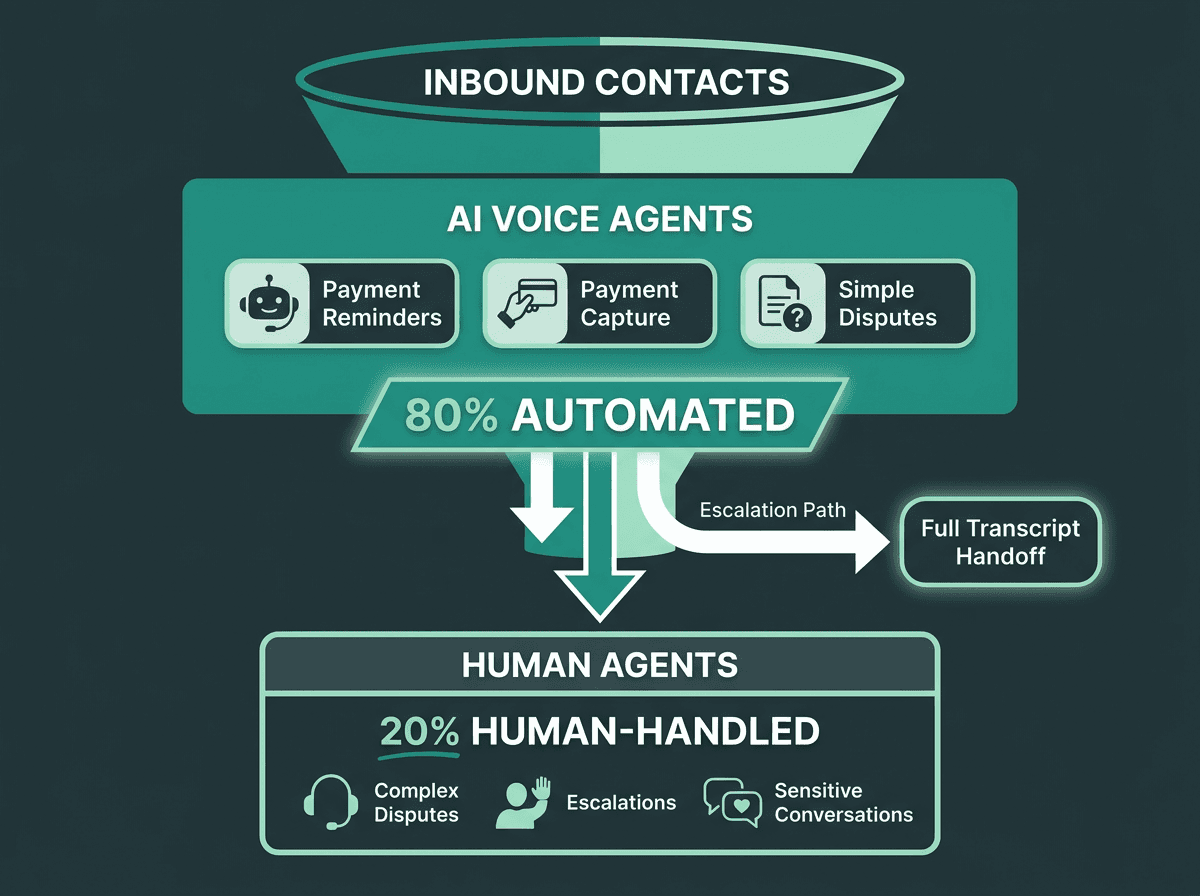

Human-AI Collaboration: Where the Hybrid Model Wins

AI voice agents absorb high-volume routine contacts, freeing human agents for complex escalations and sensitive cases.

Many organizations adopt a hybrid model where AI handles routine interactions while human agents manage complex disputes, escalations, and sensitive conversations. The split is pragmatic: AI covers volume, consistency, and availability; humans handle judgment, empathy, and the cases that do not fit the template.

That changes how you should design the product. Escalation needs to be a first-class path, not a last resort hidden behind a maze. If the agent detects frustration in the customer's voice, hears a legal threat, or runs into a scenario outside its scope, it should transfer immediately and include the full transcript for the receiving agent. A warm handoff keeps the efficiency of automation while lowering brand and compliance risk.

Common Misconceptions About AI Voice Agents in Collections

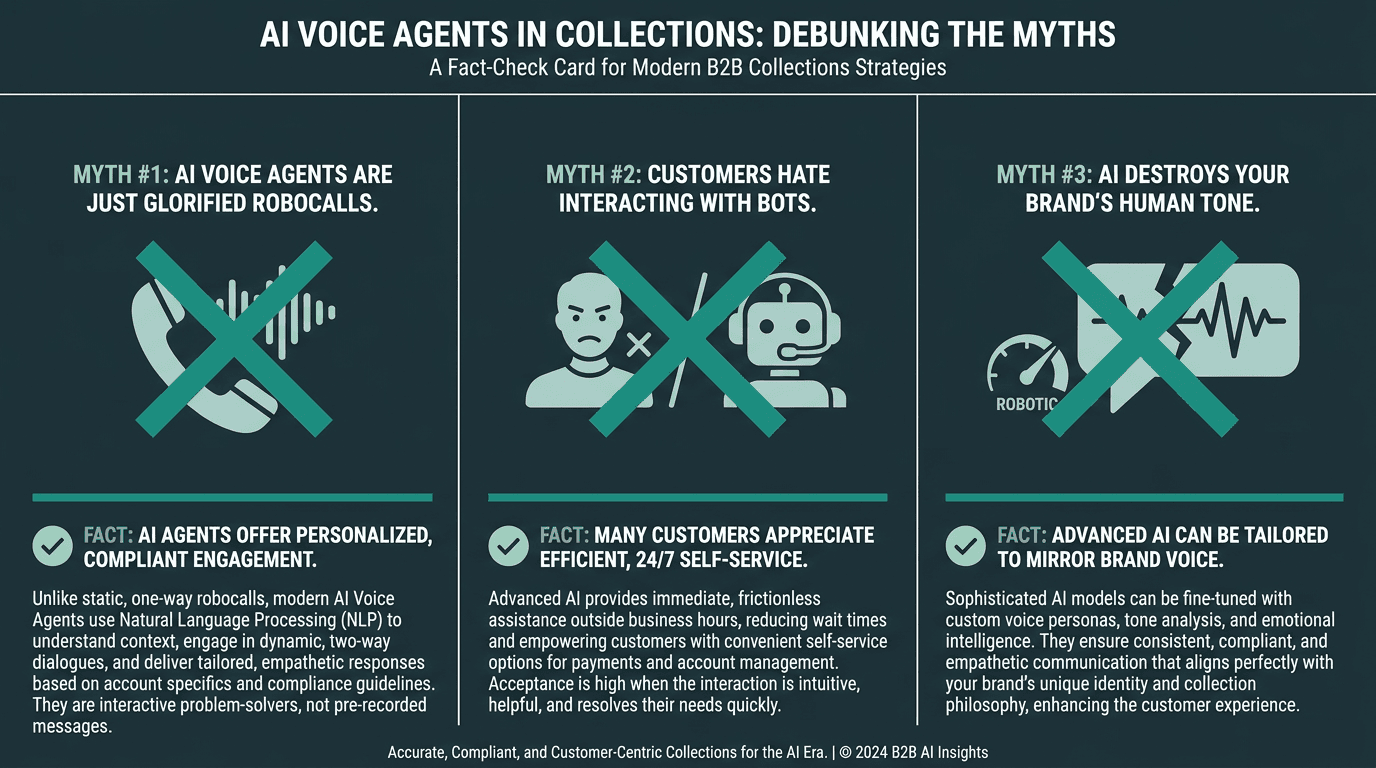

Misconception 1: AI voice agents are just sophisticated robocalls. That comparison collapses two very different things into one label. A classic robocall plays a recording and cannot respond to what the person says. An AI voice agent runs a two-way conversation, adjusts to the customer's responses, handles objections, and can complete a transaction. The FCC's 2024 TCPA ruling covers both categories, but the capability, and the experience for the person picking up, is not the same.

Misconception 2: Customers will always reject talking to an AI. In practice, acceptance is situational and heavily dependent on execution. If the call is clear about what it is, responds quickly, sounds natural, and resolves the issue fast, many customers will take that over waiting on hold. The backlash tends to come from the obvious failures: tinny audio, awkward silences, and agents that fall apart the moment a customer deviates from the script. Those are engineering and design constraints, not proof that the channel cannot work.

Misconception 3: Deploying a voice agent means losing control of your brand tone. Collections carries brand risk by default; a voice that feels hostile or dismissive can create complaints and long-term damage. Modern voice agents can be tuned at the persona and tone level, which gives teams a way to standardize how sensitive conversations sound. The piece on how to adapt AI agents to your brand voice explains how to set communication parameters that keep calls on-brand while staying compliant.

From robocall comparisons to brand tone fears — three AI voice agent myths, fact-checked.

Key Takeaways

What you need to know about AI voice agents for collections and payments:

AI voice agents are multi-component systems that combine speech synthesis, transcription, and language understanding to run true two-way collections conversations at scale.

In the US, TCPA requirements (as clarified by the FCC in 2024) and FDCPA rules both apply to AI voice agent calls, so compliance has to be part of the architecture.

Latency and voice naturalness largely determine whether customers stay engaged or hang up.

Hybrid operations beat the extremes: using AI for routine calls and humans for exceptions often improves effectiveness.

Identity verification, consent management, and escalation paths belong in the design from day one, not as retrofits.

Tone and brand voice can be configured, which helps control how the agent communicates in a high-sensitivity collections context.

Organizations are increasingly evaluating AI voice agents to improve contact rates, operational consistency, and after-hours coverage.

The Problem This Technology Was Built to Solve

Collections teams are up against constraints that adding more headcount does not fix. Contact rates drop as people screen unknown numbers. Staffing gets more expensive while recovery rates refuse to budge. Meanwhile, compliance exposure climbs as rules tighten around when and how consumers can be reached. Human agents are costly, inconsistent, and simply not available during the hours when many customers are easiest to reach.

Voice agents go after those constraints directly. They increase contact volume without requiring the same growth in staffing. They deliver a consistent interaction on every call, which matters when compliance is not optional. They can run outside business hours. And when the underlying speech stack is low-latency with accurate transcription, the call can feel like a conversation instead of a machine reading a script.

Smallest.ai is built for this style of deployment. The Smallest.ai Voice Agents platform provides the voice and text agent infrastructure for collections and payments workflows, while the Lightning Text-to-Speech API focuses on the natural, low-latency voice quality that often decides whether a customer stays on the line. For teams moving from concept into build, how to build an AI voice agent for debt collection walks through the process.

Modernize Collections With AI Voice Agents

Collections teams need better coverage, consistent customer interactions, and reliable escalation paths without endlessly expanding headcount. Smallest.ai Voice Agents combine real-time speech recognition, natural voice generation, and workflow orchestration to help organizations automate payment reminders, promise-to-pay workflows, identity verification, and customer outreach at scale.

For organizations scaling these deployments, Smallest.ai pricing offering a usage-based model that aligns with the high-volume requirements of modern debt recovery and payment processing. This cost-effective entry point allows teams to maintain operational consistency and 24/7 coverage while controlling expenditures based on actual talk time.

Are AI voice agents legal for debt collection calls in the United States?

What happens when a customer wants to speak to a human during an AI collections call?

How does an AI voice agent verify the identity of the person it is calling?

Can an AI voice agent actually process a payment, or does it just collect information?

What is the difference between an AI voice agent and a standard IVR system for collections?