Discover how AI underwriting improves risk assessment, pricing precision, and client communication through real-time data and transparent model insights.

Underwriting has always been a balance of speed, context, and judgment. Today, that balance is breaking. Data arrives faster than teams can interpret it, and every client conversation adds another layer of complexity. The insurers staying ahead are rethinking the process itself, turning to AI underwriting powered by voice AI, conversational AI, and voice agents that make every decision more informed and every call more precise.

The AI underwriting market is expected to expand at a 26.3% CAGR, reaching USD 22.13 billion by 2033, as carriers shift from manual reviews to real-time intelligence that learns, speaks, and adapts.

In this guide, you’ll see how insurers are using AI to transform risk assessment into a living process, one where voice cloning, data interpretation, and contextual automation help underwriters move faster, decide smarter, and stay ahead of change.

Key Takeaways

AI underwriting is closing the speed gap: Models process thousands of data signals in real time, giving underwriters faster clarity across submissions and risk inputs.

Voice-driven workflows are reshaping underwriting: Voice AI captures disclosures, risk cues, and context during calls, reducing manual follow-up and improving submission quality.

Pricing accuracy is improving with contextual models: Gen AI detects complex relationships in claims and exposure data, helping teams strengthen pricing precision and portfolio decisions.

Compliance stays intact through explainable AI: Transparent reasoning, audit trails, and drift checks keep AI underwriting aligned with regulatory review and fairness requirements.

Voice AI Is Powering the Next Step in Underwriting: With voice cloning, real-time response, and multilingual coverage, Smallest.ai helps insurers scale consistent, compliant, and data-driven client interactions.

Why Traditional Underwriting Is Hitting Its Limits?

Underwriting models were built for a slower world. Today, risk signals arrive faster than rules can adjust, from telematics to behavioral data. What once depended on static judgment now requires continuous interpretation across shifting inputs.

Data Volume and Complexity Have Outpaced Human Review: Underwriters once handled tens of variables; today, thousands stream in from telematics, health records, and transactions. Manual review slows as AI underwriting systems analyze this data in real time.

Fixed Rules Can’t Capture Nonlinear Risk Patterns: Conventional rules engines miss emerging correlations and rare-event interactions. AI in underwriting continuously re-trains on new data to detect evolving risk behavior across products and markets.

Fragmented Systems Limit Contextual Accuracy: Legacy tools isolate medical, financial, and environmental data, creating gaps in risk interpretation. AI for underwriting unifies these sources into a connected, interpretable view of exposure.

Compliance and Governance Demand Real-Time Adaptation: Regulations Shift Faster Than Manual Oversight Can Track. AI underwriting insurance platforms maintain auditable decision logs and adapt validation to new compliance standards.

Client Expectations Require Instant, Informed Decisions: Speed Now Defines Trust. Gen AI in insurance underwriting allows near-instant evaluations and clarifications through conversational and voice AI systems, meeting modern client expectations while preserving accuracy.

These shifts show why underwriting teams are moving toward systems that read signals as fast as risks change, not as fast as humans can sift through them.

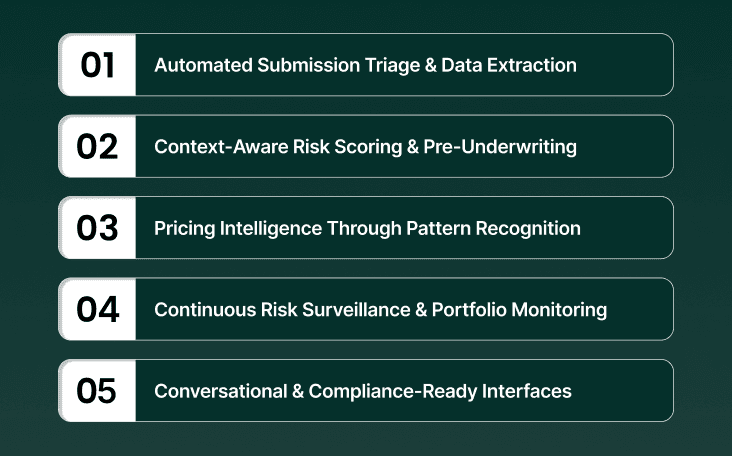

Where AI Fits into the Modern Underwriting Process

Modern underwriters face data volume that no manual process can keep up with. AI supports them by converting noise into clarity, prioritizing submissions, interpreting risk signals, and maintaining context through every stage of the policy cycle.

Automated Submission Triage and Data Extraction: Underwriting AI ingests high-volume submissions, extracts key variables from structured and unstructured documents, and ranks cases by fit, risk profile, and complexity.

Context-Aware Risk Scoring and Pre-Underwriting: AI in underwriting identifies nonlinear risk patterns across claims, exposure, and behavior, performing preliminary eligibility checks and flagging outliers for human review.

Pricing Intelligence Through Pattern Recognition: Machine learning models detect variable interactions across product lines, suggesting pricing bands aligned with observed loss frequencies and capital thresholds.

Continuous Risk Surveillance and Portfolio Monitoring: AI underwriting insurance systems track policy data post-issuance, alerting underwriters to drift, anomaly clusters, or exposure changes that affect portfolio stability.

Conversational and Compliance-Ready Interfaces: Gen AI in insurance underwriting powers voice-driven interactions, allowing underwriters to query data or audit decision logic through transparent, explainable conversations.

Discover how leading carriers are using conversational AI and real-time voice systems to modernize underwriting speed, accuracy, and compliance. Read Why Insurance Companies Need Voice Agents in 2025: The Complete Analysis.

Inside the Technology Powering AI-Driven Underwriting

The power of AI underwriting comes from how systems learn and explain. Language models, predictive pipelines, and multimodal data fusion now work together to uncover patterns that traditional analytics never could.

NLP for high-volume risk documents: Underwriting AI interprets medical files, legal notes, inspection reports, and other unstructured inputs to surface risk cues with precision.

Predictive and probabilistic risk modeling: Models detect nonlinear relationships across claims, demographics, exposures, and behavior to produce real-time probability scores.

Scenario simulation with Gen AI: Gen AI projects potential claim paths and policy outcomes under varied conditions, giving underwriters forward-looking risk visibility.

Multimodal learning with continuous updates: Systems learn from text, numbers, and images while refining accuracy through feedback loops tied to real underwriting decisions.

Real-time scoring and explainable interfaces: Latency-optimized scoring engines deliver instant outputs, and voice AI allows underwriters to query reasoning verbally for audit-ready clarity.

Conversational Interfaces via Voice AI: When paired with real-time systems like Smallest.ai, underwriters can query models verbally, receive spoken summaries, and cross-check insights on the spot.

Together, these systems create an underwriting engine that learns continuously and responds at the same speed at which new risk signals appear.

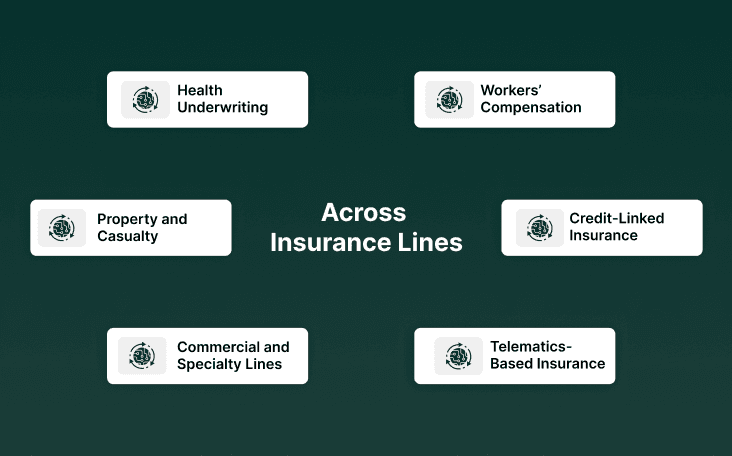

Real-World Use Cases Across Insurance Lines

The real proof of AI underwriting lies in real-world deployment. Across health, auto, property, and commercial lines, AI systems are redefining how underwriters assess, validate, and communicate risk in real time.

1. Life and Health Underwriting

AI helps underwriters move from static medical assessments to continuous, data-informed evaluations. It captures health indicators from multiple sources, lab reports, wearable data, and digital interactions, and communicates findings through natural, conversational interfaces.

Medical Data Extraction: Underwriting AI scans reports, summarizing relevant health metrics instantly for underwriter review.

Predictive Health Scoring: AI underwriting insurance models correlate lifestyle, vitals, and history to project probable claim outcomes.

Voice AI Collaboration: Underwriters use voice agents to query applicant histories or request on-demand medical summaries in real time.

2. Property and Casualty (P&C)

From flood maps to telematics, P&C underwriting produces enormous data variability. AI for underwriting processes real-time inputs to flag anomalies, quantify exposure, and communicate insights conversationally across teams.

Dynamic Risk Detection: Underwriting AI identifies exposure shifts from weather patterns, local claims data, or asset movements.

Geospatial and Image Analysis: AI underwriting models interpret satellite or drone images to assess property conditions and estimate repair risk.

Conversational Reporting: Voice agents generate instant spoken updates for field assessors or regional underwriters.

3. Commercial and Specialty Lines

These policies involve complex multi-party exposures. AI and underwriting platforms bring structure to data from contracts, inspection documents, and client communication logs.

Document Parsing: AI in underwriting extracts key obligations, coverage limits, and exclusions from lengthy submissions.

Pattern Recognition: Underwriting AI detects claim frequency anomalies or correlated exposures across regions.

Voice Collaboration: Teams discuss flagged risks through conversational AI interfaces, creating faster consensus across departments.

4. Auto and Telematics-Based Insurance

Connected vehicles generate data every few seconds. AI converts this into behavioral risk profiles, helping underwriters price policies dynamically.

Driver Behavior Analysis: AI underwriting models quantify acceleration, braking, and speed variance to predict claim probability.

Adaptive Premium Logic: Underwriting AI adjusts premium tiers automatically as driving data changes.

Real-Time Agent Interactions: Voice AI systems notify underwriters when outlier behaviors trigger potential policy adjustments.

5. Financial and Credit-Linked Insurance

Credit-based underwriting benefits from AI’s ability to identify fraud risk and validate income or transaction legitimacy through real-time data streams.

Anomaly Detection: AI underwriting insurance models catch irregular cash flows or repayment delays indicative of higher risk.

Portfolio Stress Testing: Underwriting AI runs simulations on economic conditions to model exposure volatility.

Voice Agents for Audit Queries: Underwriters can ask conversational AI to summarize exposure shifts or client payment history instantly.

6. Workers’ Compensation and Employer Liability

AI underwriting here focuses on contextual understanding of workplace safety, claim recurrence, and job-type correlations.

Incident Correlation: AI in underwriting connects injury patterns with role-specific exposure data.

Risk Classification: Underwriting AI groups employers by behavioral and historical claim data, not just industry codes.

Voice-Based Review: Claims and underwriting teams discuss flagged anomalies via real-time voice interfaces for faster assessment.

Give your underwriting teams a voice that works as fast as your data. Build, test, and deploy lifelike voice agents with Smallest.ai’s Voice AI Suite, from real-time underwriting calls to automated client interactions across 16+ languages. Book a demo!

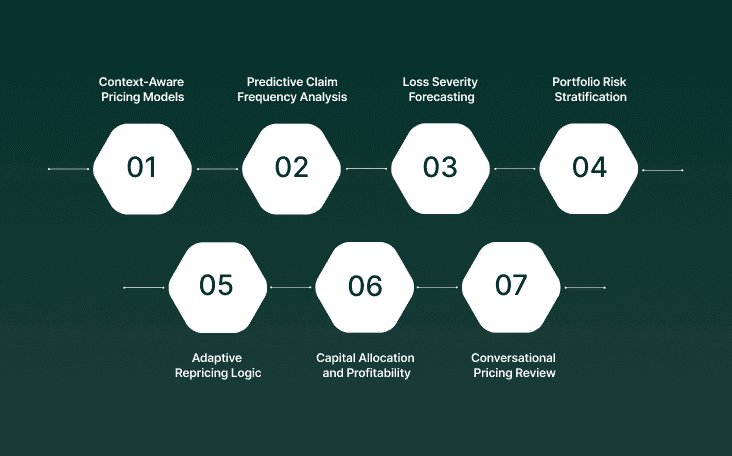

How AI Improves Pricing Accuracy and Portfolio Profitability

Pricing accuracy depends on understanding relationships that are rarely linear. AI models identify subtle patterns across claims and exposure data, giving underwriters a clearer view of profitability across portfolios and time horizons.

Context-Aware Pricing Models: AI underwriting systems connect structured and unstructured inputs, medical data, telematics, and client interactions, to produce risk-adjusted pricing with tighter variance control.

Predictive Claim Frequency Analysis: Underwriting AI surfaces hidden correlations in historical and external datasets, improving claim probability forecasts before they distort portfolio ratios.

Loss Severity Forecasting: Machine learning models evaluate severity distributions, using live market and behavioral indicators to anticipate capital exposure more accurately.

Portfolio Risk Stratification: AI for underwriting segments' portfolios by volatility and exposure overlap, providing early visibility into concentration risk before renewal cycles.

Adaptive Repricing Logic: AI underwriting insurance systems run real-time monitoring across telematics and market signals, flagging when pricing no longer aligns with underlying risk conditions.

Capital Allocation and Profitability Tracking: Underwriters gain model-backed guidance on where to expand or retract capacity, aligning capital with actual exposure data rather than projections.

Conversational Pricing Review via Voice AI: Voice AI agents allow underwriters to question model output, “Why did this risk move tiers?”, and receive clear, audit-traceable explanations instantly.

See how leading insurers are transforming client engagement, underwriting accuracy, and post-call intelligence with real-time voice systems. Read Conversational AI for Insurance: Uses, Benefits, and Key Challenges.

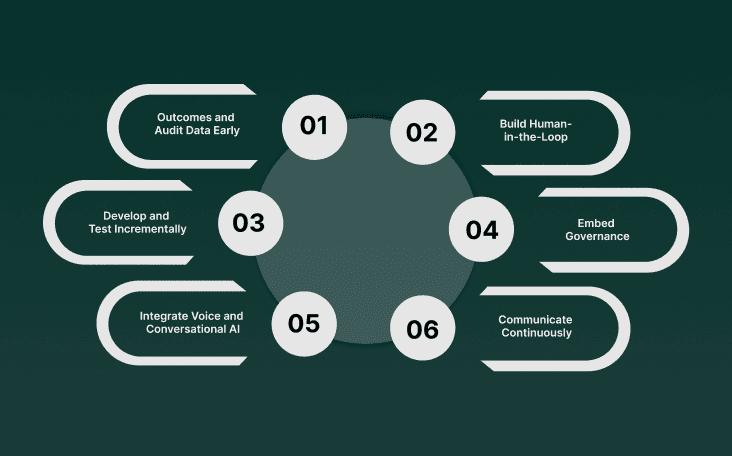

A Practical Roadmap to Implement AI in Underwriting

AI adoption is a measured progression. Teams that begin with focused pilots, validate outcomes, and embed transparency from day one achieve sustainable, compliant results that scale confidently across business lines.

Define Outcomes and Audit Data Early: Set specific targets, faster quote turnaround, or reduced loss ratio variance, and evaluate if existing data supports them. AI in underwriting depends on structured, consistent, and privacy-compliant data from the start.

Build Human-in-the-Loop Foundations: Underwriting AI succeeds when experts supervise learning cycles. Underwriters review anomalies, confirm training accuracy, and set confidence thresholds to maintain decision integrity.

Develop and Test Incrementally: Start with one product line, measure results, and adjust. Expanding AI for underwriting across portfolios should follow evidence, not assumptions, using proven metrics of precision and fairness.

Embed Governance and Compliance Frameworks: Integrate audit logging, fairness checks, and consent management into every model release. Governance is a design principle, not a final step.

Integrate Voice and Conversational AI Tools: Voice AI gives underwriters real-time access to insights, asking, “Why did this premium shift?” or “Which factors raised exposure?” and receiving clear, audit-friendly answers instantly.

Monitor, Train, and Communicate Continuously: AI underwriting insurance systems must be revalidated regularly for drift and transparency. Use conversational summaries to share results across pricing, risk, and compliance teams, turning data into shared understanding.

This approach gives underwriting teams a clear path forward, where each step builds confidence, clarity, and collaboration as AI becomes part of everyday decision cycles.

Common Roadblocks and How to Overcome Them

Most AI underwriting challenges are structural rather than technical. Gaps in data quality, oversight, and adoption slow progress. Solving them requires continuous validation, transparent reasoning, and shared accountability between systems and people.

Roadblock | Impact on AI Underwriting | How to Overcome It |

|---|---|---|

Fragmented or Low-Quality Data | Inaccurate risk models and inconsistent pricing outcomes. | Standardize data inputs, enforce quality checks, and run periodic data audits before retraining. |

Over-Automation Without Human Oversight | Loss of contextual judgment, higher compliance risk. | Keep human review at decision checkpoints to validate outputs and adjust confidence thresholds. |

Model Drift and Hidden Bias | Gradual drop in model accuracy, untracked pricing deviation. | Set up continuous monitoring and retrain using time-stamped, diversified data. |

Limited Underwriter Adoption | Low trust in AI outputs; reliance on legacy methods. | Use voice AI to explain model logic in real time and support natural underwriter interaction. |

Compliance and Audit Gaps | Regulatory delays and lack of model transparency. | Maintain traceable logs for every model decision, including input data and parameters. |

Poor Cross-Team Coordination | Disconnected insights between pricing, risk, and compliance teams. | Share voice-driven summaries for unified visibility and aligned decision-making. |

When these obstacles are managed as part of the process rather than as last-minute surprises, AI underwriting delivers results that teams can trust and build on.

Improving Risk Conversations and Client Calls with Smallest.ai’s Real-Time Voice AI

Every underwriting decision starts with a conversation. Smallest.ai’s real-time voice AI brings structure to those exchanges, capturing insights, summarizing risk cues, and feeding accurate data back into underwriting workflows as they happen.

Real-Time Conversational Intelligence: Voice agents capture disclosures, context shifts, and risk cues during live calls, giving underwriters cleaner inputs without post-call delays.

Consistent Client Interactions with Voice Cloning: Custom voice profiles maintain brand tone across regions and product lines while scaling high-volume underwriting conversations.

Instant Risk Summaries and Clarifications: Conversational AI interprets speech patterns, missed details, and emotional cues and delivers concise summaries that support faster underwriting decisions.

Low-Latency, Multilingual Communication: Lightning Voice AI allows natural two-way conversations in under 100 milliseconds across 16-plus languages for global underwriting teams.

Workflow Integration with Secure Post-Call Intelligence: Voice AI logs transcripts, flags risk indicators, and provides sentiment analysis while meeting SOC 2 Type II, HIPAA, and PCI requirements.

The result is a call experience that feeds underwriters the context they need while keeping every interaction accurate, consistent, and ready for review.

Final Thoughts!

Underwriting is shifting from static assessment to dynamic interpretation, where insight evolves with every data point. AI underwriting gives insurers that agility, analyzing live inputs, surfacing hidden risk relationships, and creating a consistent feedback loop between data and human expertise. With voice interfaces and adaptive models, AI underwriting turns every policy, claim, and client conversation into a learning system that continuously strengthens pricing accuracy and risk prediction.

Smallest.ai brings this intelligence into real-time communication. Its voice AI, conversational AI, and voice agents help underwriters capture and interpret information as it happens, turning complex exchanges into structured, auditable insights.

With voice cloning, insurers maintain brand consistency while scaling personalized engagement across markets. The result is faster, more confident underwriting powered by intelligent conversations that work as hard as your data.

Book a demo to experience how Smallest.ai elevates every underwriting interaction into a measurable advantage.

FAQs About AI Underwriting

1. How can AI underwriting adapt to sudden market shifts like natural disasters or regulatory changes?

Most underwriting AI systems include adaptive retraining pipelines that ingest external data, such as weather, inflation, or legal updates, to recalibrate pricing and exposure models without full rebuilds. This keeps AI in underwriting aligned with live risk conditions.

2. What role does conversational data play in training underwriting models?

Voice interactions and recorded calls contain behavioral and linguistic cues that improve intent prediction. When processed by Gen AI in insurance underwriting, this data helps detect early signs of fraud, hesitation, or policy misalignment, adding a new behavioral dimension to risk scoring.

3. Can AI for underwriting support reinsurance negotiations or portfolio transfers?

Yes. Advanced systems use predictive analytics to quantify aggregated exposure and simulate stress scenarios. AI underwriting insurance models provide reinsurers with data-backed confidence in risk distribution, improving pricing accuracy during treaty negotiations.

4. How does AI and underwriting intersect with ESG (Environmental, Social, Governance) risk assessment?

Emerging frameworks integrate ESG metrics into AI underwriting pipelines. For instance, underwriting AI models may factor in climate exposure or governance data when assessing long-term asset portfolios, helping insurers align profitability with sustainability mandates.

5. What skills will underwriters need as AI adoption deepens across insurance lines?

Underwriters will need literacy in AI underwriting logic, understanding feature attribution, drift detection, and conversational query systems. The future underwriter won’t code models but will question and refine them through human-AI collaboration.