AI voice APIs for fintech compliance: recording, retention, PCI redaction, audit logs, and consent workflows shaped by MiFID II and FINRA Rule 3170.

A voice API for fintech is a programmable layer that captures, processes, transcribes, and routes spoken interactions inside financial products, while honoring the recording, retention, and data-handling rules set by regulators like FINRA and the PCI Security Standards Council. It is not speech recognition duct-taped onto a banking app. It is voice infrastructure designed to behave correctly under compliance constraints.

Financial services firms live under regulatory scrutiny in a way most industries never have to. As voice becomes normal across trading desks, customer support, and payment flows, the compliance obligations attached to those conversations expand right along with usage. If you are deploying voice at scale, you need a clear view of what a voice API is doing inside a regulated stack, not just what it can demo.

Why Fintech Compliance Makes Voice Infrastructure Different

In most sectors, voice is a convenience layer: faster than typing, easier than forms. In fintech, voice is a regulated channel. Spoken instructions can move money, trigger trades, or authorize payments, which means the record of that conversation can carry legal and supervisory weight. That single fact changes what "good" looks like for a voice API.

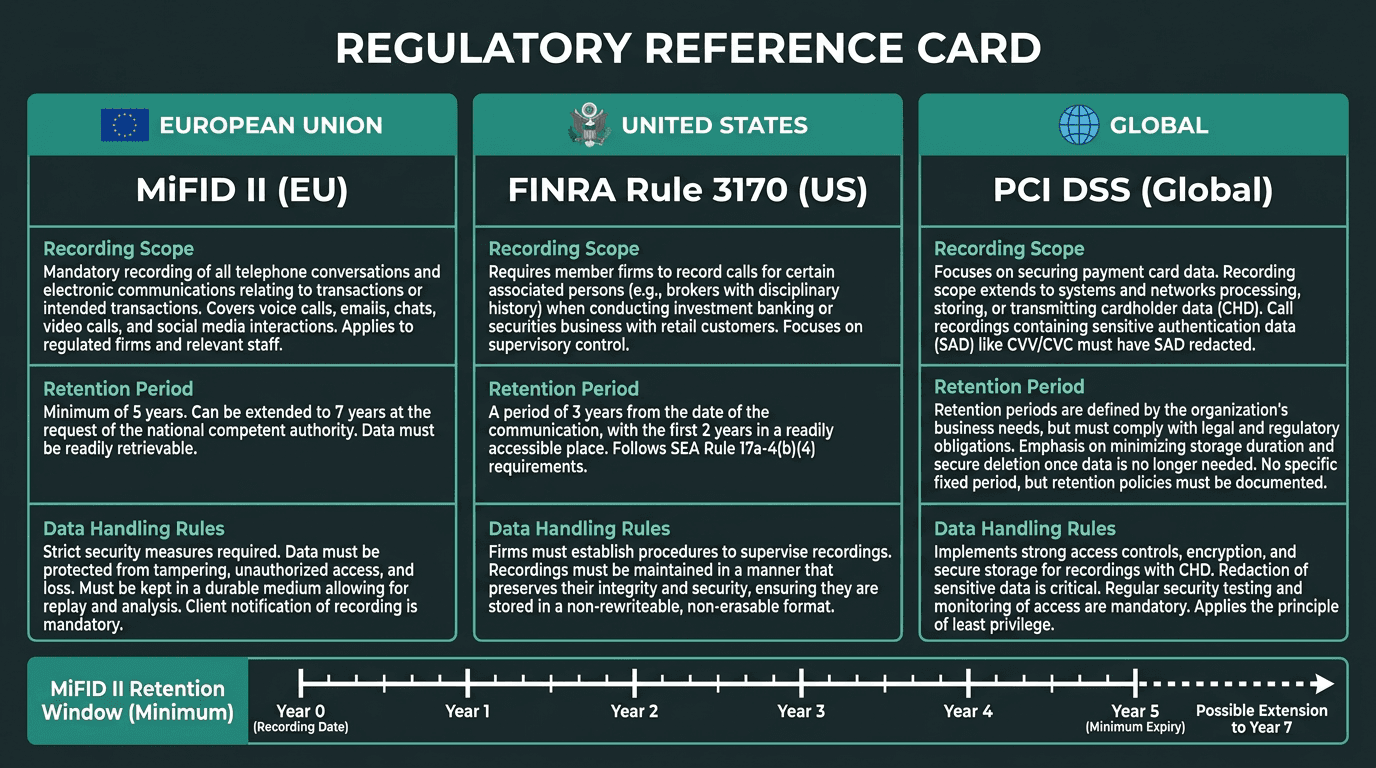

Under the EU's MiFID II regulation, firms must record voice and electronic communications relating to relevant transactions and retain those records for at least five years, with some jurisdictions or regulators requiring up to seven years.

Voice data lands right in the middle of data governance challenges: audio, transcripts, diarization or speaker tags, timestamps, and the metadata that makes it searchable later. These components are foundational for effective voice analytics and compliance monitoring. Regulators and auditors do not care that your model is accurate if you cannot retrieve the right record quickly and prove it has not been tampered with. A voice API that cannot meet those basics is not "missing features". It is introducing risk.

A side-by-side breakdown of key voice compliance obligations under MiFID II, FINRA Rule 3170, and PCI DSS.

What a Compliant Voice API Actually Does

Compliance-grade voice APIs do far more than convert speech into text. They are typically a stack of capabilities, and each capability exists because a regulation (or an auditor) expects a specific behavior from your system.

Functional Layer | What It Does | Regulatory Obligation It Serves |

|---|---|---|

Call Recording & Capture | Captures full-call audio with timestamps and structured metadata | MiFID II 5-year retention, Applicable FINRA call-recording and supervision requirements |

Speech-to-Text Transcription | Turns audio into searchable text, live or after the call | Audit trail creation, eDiscovery readiness |

PII & Sensitive Data Redaction | Finds and masks card numbers, CVV codes, SSNs in transcripts and audio | PCI DSS, GDPR, CCPA |

Speaker Identification | Labels who spoke each segment of the conversation | Dispute resolution, supervision requirements |

Secure Storage & Access Controls | Encrypts recordings in transit and at rest, with role-based access | Data governance, breach notification laws |

Audit Trail Generation | Generates tamper-evident logs for access and changes to recordings | Regulatory examination readiness |

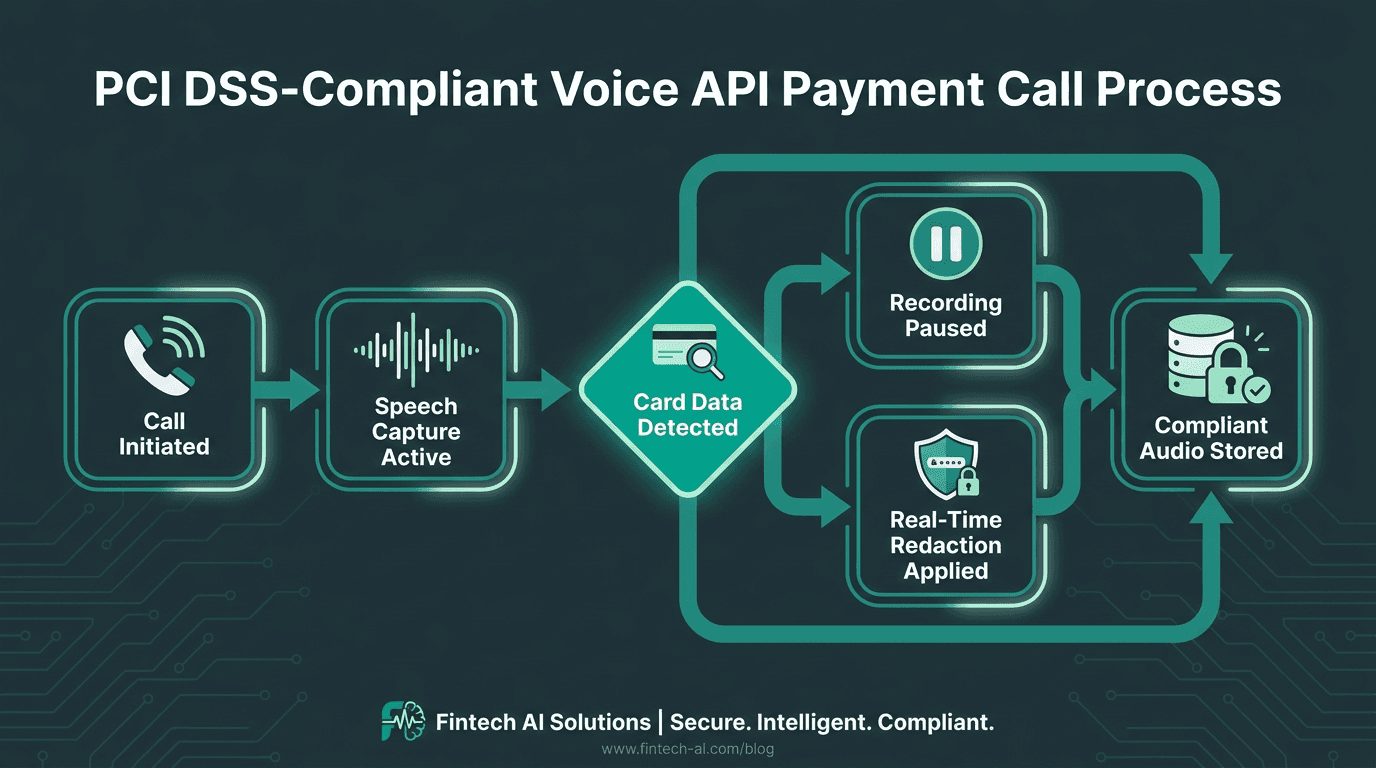

PCI DSS around sensitive authentication data is where teams get tripped up, because "we encrypt recordings" sounds reassuring and still fails the requirement. The PCI Security Standards Council guidance explicitly prohibits storing sensitive authentication data such as CVV2 codes after authorization, even if that data only exists inside an encrypted audio file. So if your voice workflow touches payments, your API needs a mechanism to pause recording during card capture or apply real-time redaction before anything ever hits storage. Encryption is still necessary. It just is not the escape hatch people hope it is.

A compliant voice API must pause or redact card data before it ever reaches storage — encryption alone does not satisfy PCI DSS.

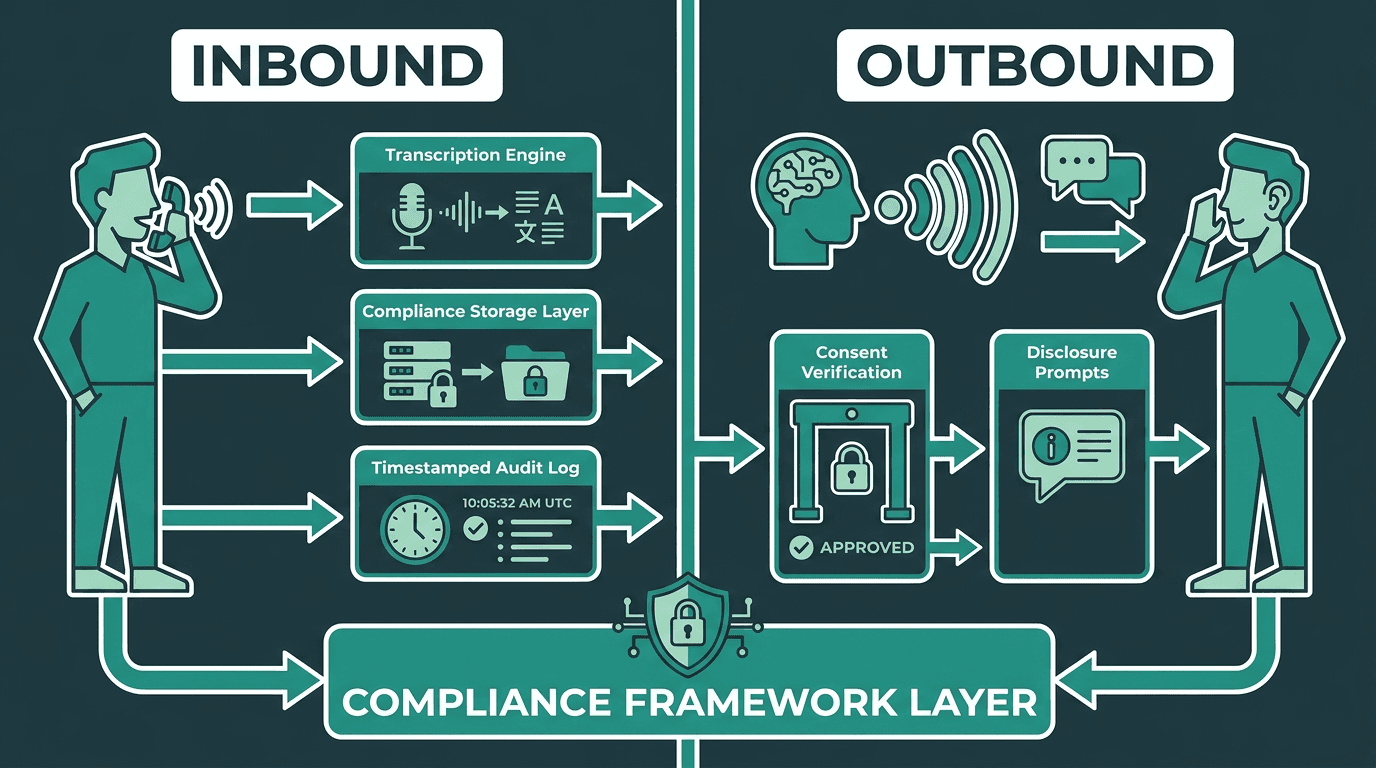

The Two Directions Voice AI Flows in Fintech

Fintech voice systems move in two directions: you either ingest customer speech, or you generate speech back to the customer. That seems obvious until you map compliance requirements to each path. The obligations are not symmetric, and mixing them up tends to produce brittle architecture.

Inbound: Capturing and Transcribing Customer Voice

Inbound flows cover what customers say into your systems: calls to a trading desk, banking IVR interactions, or disputes handled over the phone. The compliance priority here is capture fidelity and disciplined storage. You need speech-to-text APIs that handle financial terminology, accented speech, and messy phone audio without dropping the words that later become the subject of a complaint or an investigation. In a regulated workflow, transcription errors are not just a UX issue; they can change the meaning of an instruction, and that is where legal exposure starts.

If you are building a transcription pipeline that has to survive audits, AI transcription for legal and compliance teams lays out the accuracy, security, and audit trail expectations that separate a production system from a proof of concept.

Outbound: AI-Generated Voice in Customer Interactions

Outbound flows are the opposite direction: AI-generated speech delivered to customers through payment reminders, fraud alerts, account notifications, or other use cases handled by AI voice agents for BFSI. Here, the compliance center of gravity shifts toward disclosure and consent. Many jurisdictions expect customers to be told they are interacting with an automated system. Some environments also require explicit consent before recording starts. In practice, that means disclosure prompts and consent gates need to be part of the workflow logic your API supports, not a script someone pasted into a call center runbook after the fact.

Inbound and outbound voice flows carry distinct compliance obligations in financial services.

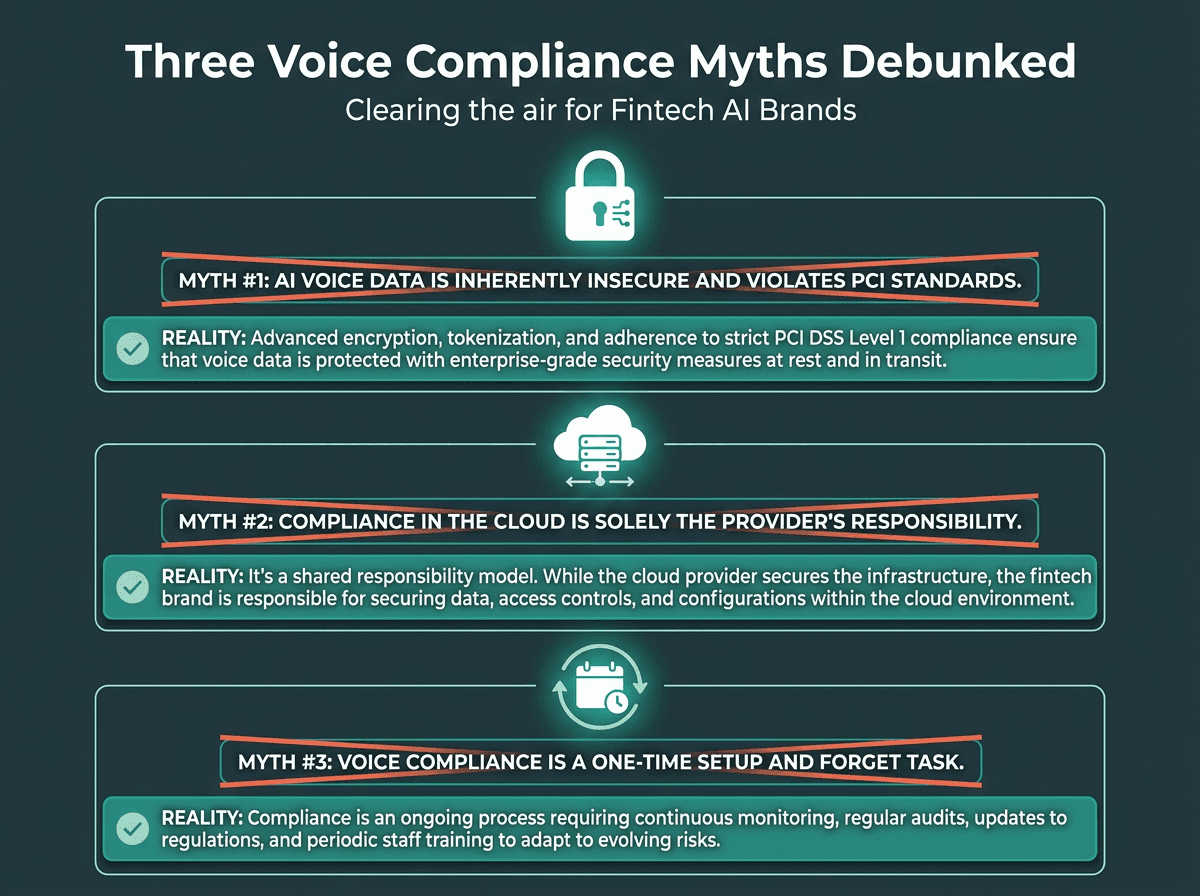

Common Misconceptions About Voice APIs and Financial Compliance

When fintech teams start shopping for voice infrastructure, the same three misconceptions keep resurfacing. Each one sounds reasonable until you run it through an audit or a PCI review, and then it becomes an expensive re-architecture.

Misconceptions that lead fintech teams astray:

"Encryption means we're PCI compliant." Encryption is table stakes, but it does not make you compliant on its own. PCI DSS forbids storing sensitive authentication data after authorization in any form, including encrypted audio. The correct design is to prevent that data from being stored at all.

"Our cloud provider handles compliance." Cloud vendors can provide compliant primitives, but they do not own your application behavior. How your voice API captures, routes, redacts, and stores data sits squarely in your responsibility under shared responsibility models.

"Compliance is a one-time implementation." Regulations move, and so do interpretations. MiFID II has been amended, PCI DSS moved from version 3.2.1 to version 4.0, and AI-specific guidance is emerging across jurisdictions. Voice deployments need recurring compliance reviews, not a single launch checklist.

Encryption, cloud responsibility, and one-time setup are the three most costly **voice API for fintech** compliance myths.

Voice Fraud Detection: The Emerging Compliance Frontier

Compliance is not limited to recording and retention. Regulators are paying closer attention to the integrity of voice channels, because voice has become a practical route for fraud. Synthetic voice, spoofing, and deepfake audio are now documented threats in financial services. In high-value transaction settings, the ability to spot altered or AI-generated speech in real time is starting to look less like an optional security enhancement and more like a baseline expectation.

A core part of this is identifying synthetic or altered speech in real time, which matters more as regulators begin addressing AI-enabled fraud over voice.

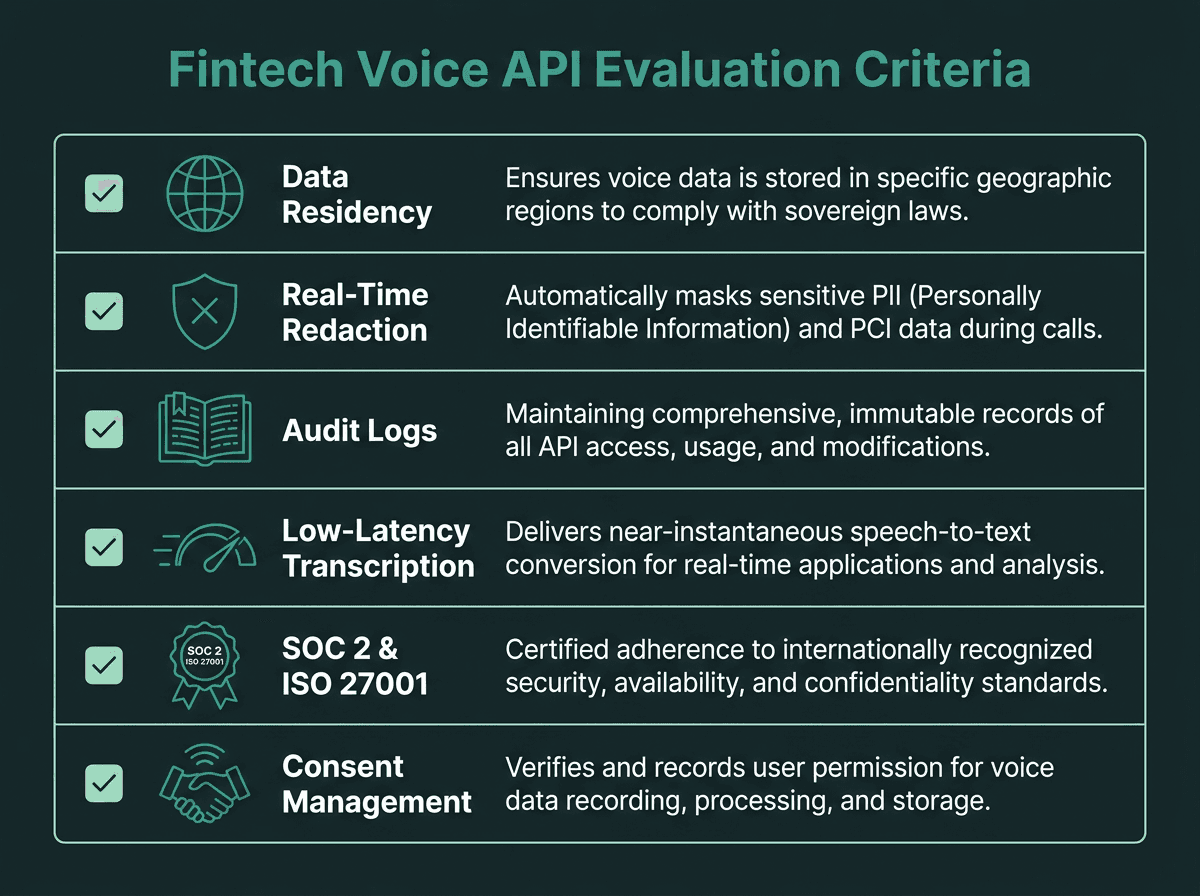

What to Look for in a Voice API Built for Regulated Environments

Most voice APIs are built for general developer use cases, not regulated ones. In fintech, the evaluation rubric changes: security posture and operational controls outweigh shiny feature demos. Data residency options can matter more than raw latency numbers when you are dealing with cross-border constraints. What distinguishes consumer-grade voice tooling from enterprise-grade infrastructure is the security architecture.

Non-negotiable criteria for a fintech-grade voice API:

Data residency controls: Support for choosing where audio and transcript data lives, which is central to GDPR and cross-border transfer compliance.

Real-time redaction: Masking card numbers, PINs, and other sensitive data before storage, rather than trying to scrub it later.

Tamper-evident audit logs: A complete record of access, playback, and modifications, structured so it cannot be quietly altered.

Low-latency transcription: On trading desks and live monitoring use cases, latency has to be low enough to act on while the call is still happening.

SOC 2 Type II and/or ISO 27001 certification: Common security assurance frameworks for vendors handling regulated financial data.

Consent management hooks: API-level support for consent workflows, not a hand-wave that says "you handle consent" in documentation.

Six criteria that separate a compliance-ready voice API from a general-purpose one.

Build Voice Workflows That Hold Up Under Audit

In regulated environments, voice infrastructure has to do more than transcribe and synthesize speech. Recording controls, audit trails, consent workflows, data handling, and low-latency processing all need to work together. Smallest.ai provides low-latency speech infrastructure for voice agents and voice-enabled workflows. Organizations operating in regulated environments should evaluate how any platform's security controls, deployment model, certifications, and compliance capabilities align with their own regulatory obligations. The underlying speech stack, including Lightning for text-to-speech and Pulse for speech-to-text, targets low-latency, high-accuracy processing that live-call monitoring and supervision rely on.

Book a Voice Agents Demo to See How Smallest.ai Fits Regulated Voice Workflows

Key Takeaways

What fintech teams need to understand about voice APIs and compliance:

A voice API for fintech is compliance infrastructure, not a speech recognition add-on.

MiFID II requires five-year retention of voice communications that could lead to a transaction.

FINRA Rule 3170 mandates call recording for certain broker-dealer categories to prevent fraud.

PCI DSS prohibits storing sensitive authentication data in audio recordings, even if they are encrypted.

Inbound and outbound voice flows create different compliance obligations and should be designed accordingly.

Voice fraud detection, including synthetic speech identification, is becoming a regulatory expectation.

Data residency, real-time redaction, and tamper-evident audit logs are non-negotiable in regulated deployments.

Compliance is an operating requirement that persists after launch, not a one-time milestone.

What does a voice API for fintech need to do that a standard voice API does not?

Does encrypting voice recordings satisfy PCI DSS requirements?

How long do financial firms need to retain voice recordings under MiFID II?

Can AI-generated voice agents be used in regulated fintech environments?

What is the difference between call recording compliance and voice data governance?